Life

Insurance & Mortality Table

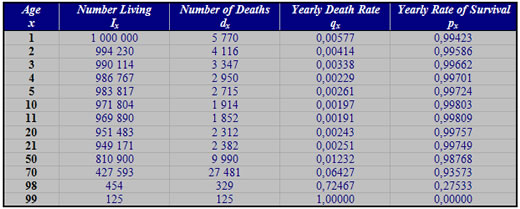

A mortality table

is essentially a record, based on past experience, that

shows the number of persons living at successive ages out

of an original group of given size. For convenience, the

original group is usually taken as 100 000 or 1 000 000

at age one. The table also includes information other than

the number of persons living at successive ages.

One of the widely

used mortality used at the present time is the Commissioner

1941 Standard Ordinary Mortality table (usually referred

to as the CSO table).

If we denote by

Ix the number of persons from the original group who live

to attain the age x, then the table shows that I5 = 983

817, I50 = 810 900 etc. Clearly the numbers that die in

any year can be obtained as the difference living at consecutive

ages. Thus

I10-I11=971804-969890=1914

persons died between

the ages of ten and eleven. If we denote by dx the number

of persons in the original group that attain age x but die

before reaching age x+1, then clearly

dx=Ix-Ix+1

Thus d50

= 9 900 means that 9 900 persons out of the original 1 000

000 died during their fiftieth year of life. Since Ix

persons attain age x and Ix+1 of these also reach

age x+1, the probability

Px=

Ix+1 / Ix

is

called the probability of survival for persons of age x.

Likewise, since dx persons die between the ages

x and x+1, the probability

Qx=

dz/Ix

is

called the rate of mortality, or death probability, for

persons of age x. The mortality tables is the foundation

of life insurance and life annuities and is therefore of

fundamental importance. It should be clear that a mortality

table based on a given group will not agree exactly with

another table based on a different group. For example, wide

differences are found in the rate of mortality according

to race, sex, occupation, standard of living and various

other factors. Consequently, there are numerous mortality

tables in actual use, and many of these revised from time

to time as medical science progress and general health conditions

improve, thus increasing the span of life. Most life insurance

companies use at least two mortality tables: one for life

insurance and a different one for life annuities. For if

people die more rapidly than predicted by the mortality

table, the company pays out faster on insurance policies

and life annuities.

The

fundamental principle that makes life insurance and life

annuities sound is that persons of a given class do tend

to die with approximately the same regularity as indicated

by a mortality table made up of such group.

Example:

The graduating class of a university contained 500 students

aged twenty-one. According to the CSO table, how many of

these will be alive to celebrate their fiftieth reunion

of their class?

Solution: The question is, essentially,

how many of these 500 students will live to attain the age

of seventy-one. The CSO table gives I21 =949 171 and I71

=427 593. Consequently the expected number is

500x(I71/I21)=500x(427593/949171)=225