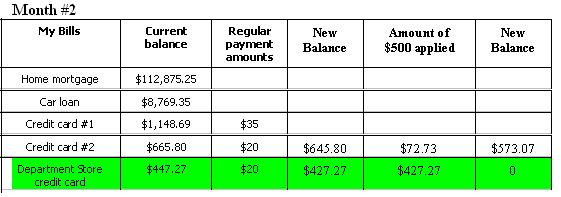

Note: new interest charges would be added to the above balances. For the Department store credit card: last balance was $438.18 plus $9.09 in interest charges equals current balance of $447.27. For the credit card #2 we added $5.45 in interest charges to the balance after our last payment which was $660.35.

Our bills are really starting to deplete! We have just knocked off another bill from our list! We can now take the $20 minimum payment we were paying towards it and add it to our $500. We now have $520 to apply to our debts next month.

From the chart above we can see that the credit card #2 balance is left at $573.07 before our next month�s interest charges are added. We will be able to completely pay this off next month by either working a few extra hours next month or by cutting down one of our expense categories in our budget.

After next month we will only be left with our house loan, car loan, and just one credit card! We will now have $540 to apply towards our debt since we will no longer need to make that minimum payment any more. Continue to follow this same method until you have paid off all of your debt. Once you have paid off all of your credit cards start sending the money towards paying off your car. Just think of how much extra money you will have!

A note about residual finance charges. Residual finance charges represent the finance charges from the last time you were charged them until the day your new payment is received. For instance, you receive your credit card bill and send in a payment for the entire balance. Then next month you receive another bill from the same company for a finance charge. You thought it was paid off. Based on the terms and conditions of your credit card agreement, these would be valid charges. However, you may be able to call customer service and see if they might be able to waive them for you. Policies vary between companies on waiving finance charges. Some companies are pretty lenient while others are not. Another bargaining chip you have is whether or not you will keep the credit card account open once it is paid off. For companies with more stringent policies on waiving finance charges this may help you. I worked for many years in the credit card industry including working as a customer service representative answering phone calls. I would always waive these for customers in order to keep an account. |