|

|

INSTITUT TADBIRAN AWAM NEGARA |

|

| Balanced scorecard: theoretical perspectives and public management implications | ||

| Age Johnsen | ||

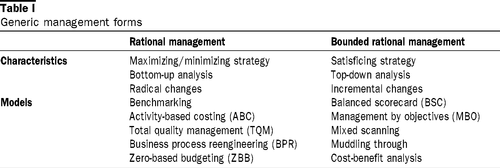

IntroductionThe purpose of this paper is to identify relevant theoretical perspectives on and point to public management implications of the balanced scorecard (BSC). The BSC has aroused a large and growing literature, see for instance Otley (1999) and Nørreklit (2000). The BSC is now widely diffused in business and probably also to some degree in public management. The BSC's acclaimed merits and prescribed design seem to be identical for both the business and the public management contexts. The public management context has hitherto only received scant scholarly attention regarding use of the BSC. However, accounting and management models should be studied in the context that they are supposed to operate in (Hopwood, 1983). In this paper I shall argue that a uniform approach to strategy, performance measurement and performance audit in business and public management may lead to some unintended and possibly dysfunctional consequences if and when the BSC model uncritically is implemented and used in public management. The BSC is important to study because it constitutes a basic part of the proposed remedies to regain relevance in strategy and management control. In 1987 Johnson and Kaplan published their seminal and then controversial book Relevance Lost: The Rise and Fall of Management Accounting (Johnson and Kaplan, 1987). The authors claimed that relevance was lost because management accounting from the 1950s to the 1980s was driven by the procedures and cycle of financial reporting. This resulted in information coming too late, reported too aggregated, and being too distorted to be relevant for aiding managerial planning and control decisions. Fortunately, Johnson and Kaplan (1987) and colleagues also made three suggestions for improving the relevance in strategy and management accounting. These suggestions Johnson and Kaplan called identifications of paths for major innovations: In chapter 9 they addressed quality management for process control. In chapter 10 they presented a sketch of a new system for product costing which presently is known as activity-based costing (ABC). In the last chapter, 11, they proposed a model for evaluating periodic performance, "a performance measurement model for the future". This specific performance measurement system Johnson and Kaplan proposed, is now widely diffused and is known as the BSC. After Relevance Lost: ... the BSC model was elaborated upon in three papers in the widely known practitioner journal Harvard Business Review (Kaplan and Norton, 1992; 1993; 1996a). The basic scorecard model, its implementation, and its strategic use were subsequently synthesized and published as a book by the Harvard Business School Press (Kaplan and Norton, 1996b). In the later 1990s there has also been developed several modifications of the BSC model, for instance in Scandinavia. When it comes to performance measurement both in business and public management in general, there is a rich tradition (Simon, 1997; Ridgeway, 1956; Mayston, 1985; Meyer and Gupta, 1994) long before the BSC model entered the management agenda in the early 1990s. The BSC is, in this field, only a relatively recent contribution. However, in the remaining parts of this paper I shall mainly discuss the "original" BSC model. When I said earlier that the BSC has been published in practitioner-oriented outlets, I did not want to suggest that most authors in, for instance, the Harvard Business Review are not scholars or that what is published in practitioner's journals are not important, rather the contrary. In fact, Johnson and Kaplan (1987) made it explicitly clear that much of the acclaimed lost relevance in management control in the period from the 1950s to 1980s was due precisely to too much emphasis on formal modeling, for instance in agency theory, and too little emphasis on experimenting and practice. When I suggest here that, for instance, agency theory is one relevant theoretical perspective for understanding performance measurement and studies of the BSC, it is not to claim that performance measurement issues should be substituted with abstract theories or formal modeling rather than studied and developed in practice, but complemented with positive studies. I want to address managerial applications of the BSC in public management, as in local government. Albeit most managers may have associated the BSC with business strategy implementation, the BSC could also have important applications and implications for public managers. Many management innovations have their origin in public administration[1]. Furthermore, many business management models may also be rapidly diffused to public sector organizations. Thus, public management is both a large and important field for management and auditing studies and can be useful also for understanding the potential applications for the BSC. The rest of this paper is outlined as follows. In the next section I develop a framework for classifying management models based on two generic management forms. I also elaborate on the BSC in relation to this framework and explain how positive agency theory and political economy may enhance our understanding of how performance measurement functions in public management. The proceeding section discusses some recent empirical studies on performance measurement and balance scorecard applications in public as well as in business management. Furthermore, I discuss some potential managerial implications of using the BSC in public management. The study is rounded off with some cautions regarding possible pitfalls of using an unmodified BSC in public management. Theoretical perspectivesStrategy and management models are commonly described and studied as fads and fashion. Practitioners and students of management may in this respect recall earlier models forerunning or resembling the BSC, as management by objectives (MBO) and mixed scanning. Even the slogans used to market the BSC model, i.e. "(m)anagers, like pilots, need instrumentation about many aspects of their environment and performance to monitor the journey toward excellent future outcomes" (Kaplan and Norton, 1996, p. 2), are basically identical to those Drucker (1954, p. 87) used to motivate application of the MBO model, i.e. "(o)bjectives in the key areas are the `instrument panel' necessary to pilot the business enterprise". In my view, the symbolic perspective (Meyer and Rowan, 1977) on diffusion and adoption of strategic management models are far from exhaustive for understanding management models' applications and implications. For instance, even though more information is collected and displayed than are actually used in organizations, maybe in order to symbolize a modern and efficient organization, information may also be used strategically, that is: actors generate, process and communicate information in a context of conflict of interest and with consciousness of potential decision consequences (Feldman and March, 1981). Even though the BSC could have been analyzed as yet another management fashion invading business strategy and public management, it could also be analyzed based on its generic content and its practical impact hopefully without biased ideological presumptions. In this study I have focused on instrumental and political issues, as political competition, for enhancing our understanding of managerial applications of management models as the BSC. Generic management formsTable I gives a sketch of the two generic management forms with some typical management models: a "rational" management form and a "bounded rational" management form. See Bjørnenak and Olson (1999) for a different approach to unbundling management accounting innovations. Generic rational management is characterized by a maximizing strategy (or the dual problem of minimizing), bottom-up analysis and radical changes. Generic bounded rational management models, on the other hand, are typically inclined to satisfied rather than optimize, decompose analysis of problems from aggregate to lower levels, and implement only incremental changes. Typical models within this generic form of management are, for example, MBO, mixed scanning (Etzioni, 1967), Lindblom's (1959) "muddling through", and cost-benefit analysis/policy analysis (Wildavsky, 1966). While benchmarking (Camp, 1989) and the BSC are both performance measurement models, the former is here categorized as "rational" and the latter as "bounded rational". The reason for this division is that benchmarking typically aims for comparing against best practice and world leading organizations. The BSC and most other performance measurement models typically compare more modestly to an organization's history or collaborating organizations' performance. The ABC and total quality management (TQM) models are basically variants of the generic rational approach to management and organizational decision-making because they take a bottom-up approach in trying to minimize costs or optimize quality. Earlier typical models within this management form are for instance zero-based budgeting (ZBB) and the related and more recently promoted business strategy model known as business process reengineering (BPR). MBO, mixed scanning and muddling through are models that are relatively more pragmatic in their use and therefore have been categorized as bounded rational. It should be noted that management systems in practice often are a blend of different generic management models. These systems utilize different degrees of underlying dimensions as bottom-up versus top-down analysis, and radical versus incremental changes. For instance: several of the models on both sides of the rational/bounded rational dichotomy utilize certain degrees of employee participation in analysis and implementation of prescribed changes. Benchmarking may be used both in conjunction with TQM as well as with the BSC. Even though the rational models may identify the need for radical changes, these changes may be implemented incrementally. Elements of scientific management (Taylorism), which also could have been categorized as a generic rational management model, are widely used in different management models. Scientific management was also extensively used in Soviet-type, central planning models. Thus, complex organizations seem to have considerable overlap of management models in use simultaneously (Downs, 1967; Bradach and Eccles, 1989; Meyer and Gupta, 1994). The BSC modelWhat is the BSC? The BSC is a management model which is used to translate an organization's mission and strategy into a comprehensive set of performance measures that provides the framework for a strategic measurement and management system (Kaplan and Norton, 1996). There are four different scorecards in the BSC system: financial, customers, internal business processes, and learning and growth. For each firm the performance indicators must represent performance drivers in accordance with traits in the industry and firm. The BSC is claimed to be consistent with the MBO model. The MBO model (Drucker, 1954, 1976) is based on three parts:

Thus, the basic elements of the BSC model are not new. In fact, the BSC could be seen as an extension of MBO but with more emphasis on feedback on results by formal and integrated performance measurement. Drucker (1954) argued in his classic book, The Practice of Management, that management in every decision and action, in business or in public management, always should put economic performance first. Drucker also argued that the only resources capable of enlarging the firm were human resources, and that any business firm has only two basic functions: marketing (customers) and innovation. However, Drucker (1954) claimed that at that time one knew very little about productivity and was then not able to measure it, especially with the prevailing but obsolete accounting models, a theme which later was eloquently elaborated on by Johnson and Kaplan (1987). The BSC has, consistent with MBO, retained the emphasis on achieving financial objectives, focusing on marketing and customers and pursuing innovation (learning and growth). However, its measurement system comprises an acclaimed balance between financial versus non-financial, internal versus external stakeholders, and short-run versus long-run performance drivers. From this brief exposition one sees that most of the elements in the BSC were already clearly present in MBO in the 1950s, but not integrated with valid performance measurement. The BSC could therefore be viewed as a modification of, or innovation in, the much used MBO model. The BSC model is also basically equivalent to the generic form of bounded rational management because of its characteristics of using a satisfying strategy, employing top-down analyses and implementing incremental change. In my view the balanced view on management control and strategy implementation with emphasis on decision relevance is the main innovation of the BSC model. I here understand innovation in an Schumpeterian sense, that is, as putting together new combinations rather than inventing new technologies or models, which is the traditional role of an entrepreneur. Thus, the BSC presents an integrated model for how to represent the most decision relevant performance drivers for management by integrating performance indicators in the MBO model. However, there are some potential pitfalls in adopting business strategy and management models directly into public management without further considerations of possibly dysfunctional consequences (Smith, 1995; Goldsmith, 1997). For instance, the BSC presently addresses shareholders, employers and customers. But, public management is also concerned about other stakeholders, clients and citizens in particular (Pollitt, 1988). The present formulation of the BSC seems on the one hand to address learning and growth in a uniform positive vein. On the other hand, if efficiency is the primary purpose of the agency's production rather than equity or reliability (Hood, 1991), then learning how to reduce costs and hence become smaller in (budget) size may be more appropriate than growth. Growth thus is increased added value. This means that the theoretical perspectives that one chooses in studies of performance measurement may have implications for which managerial applications of the BSC one would ultimately prescribe or want to modify. Agency theoryJensen (1983), a prominent scholar within agency theory, argued that purposeful decisions could not be made without implicit or explicit use of positive theories. Unfortunately, he argued, most of the vast literature falling under the label "theory of the firm" in fact was no positive theory of the firm but a theory of markets. He recommended that studies of organizations should utilize the concept of complex contracts including performance measurement, evaluation and reward systems. Jensen called for both quantitative as well as qualitative approaches, use of "institutional" evidence as well as mathematics. However, he argued, use of mathematics may be counterproductive and especially in dealing with new and uncharted areas as organization and accounting theory. Though there may have been significant development in these areas since the early 1980s, I principally agree with Jensen and think management studies are best guided by pragmatism and a balance between formal modeling and positive studies, as well as a balance between theory and practice (cf Nelson and Winter, 1982). While much of the scholarly work in agency theory, and especially within the more formal principal-agency branch, may have been devoted to financial and individual incentives, this stream within agency theory seems to be less relevant for my project. However, the positive agency theory branch may apparently be of a relatively higher and a more immediate practical relevance with respect to understanding the BSC in a managerial context. With these considerations in mind, I want to address two theoretical perspectives on the BSC:

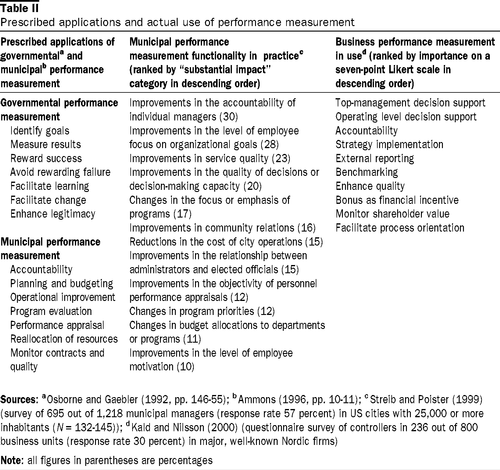

Agency theory is basically concerned with implementation of legitimate stakeholders' decisions (Jensen and Meckling, 1976; Fama and Jensen, 1983). Typical structures used in order to monitor the implementation of these decisions are work contracts, financial accounting, auditing and performance measurement. While much agency theory research has been conducted in a business management context, it should be kept in mind that the original formulations of agency theory explicitly addressed its relevance for nonprofits, voluntary and public sector organizations as well. Thus, from agency theory we learn that monitoring by performance measurement and auditing may be a versatile management instrument in implementation of legitimate stakeholders', and not only shareholders', decisions. In a well-known paper within agency theory, Kerr (1975) argued against the folly of rewarding A while hoping for B. This theme was later elaborated on by Baker (1992) in a paper on incentives contracts and performance measurement. Baker reminded us of the importance of a close alignment of agency incentives with the principal's preferences when there is asymmetric information, in order to avoid dysfunctional effects and unsuccessful implementation. Thus, agency performance measures should be aligned with the principal's values. In this respect the two concepts of political uncertainty and simultaneously multiple principals, may be fruitful for understanding managerial applications of the BSC. However, these concepts are commonly treated within the public choice, bureaucracy theory branch in political economy. Political economyThe public choice, bureaucracy branch of political economy seeks to explain the three basic questions of what bureaucrats want, how they may get what they want, and how bureaucrats can be controlled. Common answers to these questions are respectively: bigger discretionary budgets or more influence; by asymmetric information, agenda control and selective efficiency; by authority, competition, trust, or incentives (Wintrobe, 1997). According to the US political scientist Moe (1997) positive theory on bureaucracy has, in later years, largely incorporated agency theory and transaction cost analysis. In fact, much of the modern bureaucracy theory has substituted the classical frameworks of the German sociologist Weber (1947) and the American economist Niskanen (1971), with agency theory as well as with transaction costs analysis. Although Johnson and Kaplan (1987) made ample references to both agency theory and transaction cost theory, I think transaction cost theory (Williamson, 1991) is relatively more suitable in studies of activity based costing, total quality management and regulation issues (Horn, 1995), and agency theory is relatively more suitable for performance measurement issues. The argument for this distinction is this: both quality management and activity-based costing frequently analyze transactions where ownership or costs are in question, for instance in relation to contracting out and supply chain management. Performance measurement more often analyzes whole organizations and services as value chains (Porter, 1985; Rappaport, 1986; Johnsen, 1999) and where there is agreement on continuity of the service provision. While these questions often are intertwined in practice, this distinction may warrant for my discussion here. Next, I shall therefore only discuss issues relating to political uncertainty and multiple principals within agency theory. First, Schumpeter (1950), one of the intellectual founding fathers of the public choice school, introduced the concept of political competition. In a democratic system the citizens elect those representatives they want in free elections. However, these representatives do not represent the common interest directly. Instead, based on their political interest, they compete for re-election and political influence, and the outcome of this competition may serve a "common" interest. Thus, in public management the concept of strategic use of information and political competition may be closely related. However, the political system is permeated with political uncertainty (Moe, 1997). Political uncertainty means that the political representatives may lose their power, for instance in the next election. The ruling political leadership has furthermore no property rights on the political structures or programs they create. This means that any legislation, regulation or governance structure is designed such that political enemies eventually cannot use these structures in their own interests exclusively, immediately, or without substantial costs. Therefore, political institutional design may utilize multiple principals to monitor an agency (Moe, 1997) and implement performance measurement systems loosely coupled to the, at any given time, prevailing political goals of the ruling coalition (Johnsen, 1999). These protective structures prevent any or sudden change in political leadership immediately ruining the political achievements of the former political leadership. Second, the phenomenon, which Moe (1997) calls multiple principals, is usually addressed as common agency within regulation theory. In public management there is seldom one principal to control or regulate each agency. One agency has several principals simultaneously. Furthermore, the multiple principals may emphasize different aspects of the common agent's performance. The public organization's performance is therefore not easily measured and certainly not by a handful of financial indicators which do not make much sense as performance indicators in political institutions in the first place (Simon, 1997). If all the principals' ambiguous preferences and goals (Baier et al., 1986) should be operational zed in a BSC, this could lead to severe proliferation of performance indicators, to substantial measurement costs, and, furthermore, to ambiguous performance indicators with low decision relevance (Johnsen, 1999). A preliminary conclusion regarding theoretical perspectives and the BSC is that theories that explain implementation and political competition, are relevant. In this respect agency theory and public choice seem as relevant perspectives in studies of performance measurement issues. Some empirical evidenceThe BSC is, as pointed out earlier, to some degree an extended model of MBO. One may therefore assume that the BSC model in public management has at least some of the same effects as the MBO model. The MBO model has, based on 30 municipal studies reviewed in a US meta study (Rodgers and Hunter, 1992), showed that it was good for productivity improvement. A total of 70 studies also showed that the MBO model was at least as successful in the public sector as in the private sector. But, assuming a positive relationship between MBO and performance measurement is not satisfactory for a positive study. Specifically, Poister and Streib (1995) found that MBO was a traditional and widely used management tool in US local government. However, their study also documented that there was a widespread variation in how MBO was used. Fortunately, some recently published studies on the use of performance measurement in business and public management may help us in providing some more information on managerial applications of the BSC. Table II gives data on prescribed applications and actual use of performance measurement including the BSC. The first column in Table II gives prescribed applications of governmental (Osborne and Gaebler, 1992) and municipal performance measurement (Ammons, 1996). Many of the prescribed applications can be mapped in a traditional, cybernetic management control cycle of strategic planning and programming, operations, measurement, and evaluation (Anthony et al., 1984). Some of the prescribed applications of performance measurement in public management also suggest an evolutionary perspective (Nelson and Winter, 1982). Monitoring may serve in identifying goals and opportunities, reduce uncertainty by learning, select efficient routines by rewarding successes and not failures, and facilitate change. Nelson and Winter (1982) in fact used political economy and welfare theory in their discussion of evolutionary theory in public policy, including issues on monitoring and central planning. The second column gives data on how performance measurement has been used in large US municipalities. Streib and Poister (1999) reported that most of the US municipalities studied in their survey were working from organizational missions, goals and objectives, a result consistent with the prescribed use of the BSC. However, the municipal managers' efforts also tended to focus on available data, a problem which, if persistent in the longer run, may lead to low validity and hence low decision relevance. Measuring quality appeared to be an especially difficult task. The findings also suggested that municipal officials were not in agreement with the literature supporting citizen involvement in the measurement. Poister and Streib (1999) summarized their study by saying that it appeared only 40 percent or fewer made any kind of meaningful use of performance measures in their management and decision processes. Even among those cities that made substantial use of performance measurement, measures were not used in all program areas. This may indicate resistance or cost-benefit considerations regarding implementation. In fact, 45 percent indicated that they sometimes had trouble in getting managers to support their measurement systems. The survey showed that the overwhelming motivation for using performance measurement in the cities appeared to be locally generated, stemming from a desire to make better decisions and to maintain accountability to citizens and local elected officials, rather than from the need to meet state and federal reporting requirements. This latter conclusion supports the notion for avoiding studying management control systems as symbols only, and also highlights the decision relevance theme in performance measurement issues. As far as I know there has not been any systematic survey on use of the BSC model in public management, but see Brignall and Modell (2000) and Kloot and Martin (2000). The third and last column, due to lack of available data, only gives data on how performance measurement has been used at Nordic companies. Off the business units studied in Kald and Nilsson's (2000) survey of 236 Nordic companies, 27 percent used the BSC. Within two years 61 percent of the units may be using the BSC according to the answers given by the controllers in the units surveyed. If these data are representative for the future, then these data may also give some insights in potential applications of the BSC. Kald and Nilsson (2000) found in their study that the principal use of performance measurement was decision support at the top-management and operational level. They also found that performance measurement was used in benchmarking, and to enhance quality. Performance measurement did not, however, play any large role in determination of bonuses. Thus, this supports the notion that performance measurement is relatively less important in conjunction with individual financial incentives, at least in the Nordic countries, and that there are widespread overlap of management models in practice. The most important benefit of performance measurement was its contribution to a better understanding of how the business worked. Hence, performance measurement reduces uncertainty. There were several shortcomings of performance measurement such as too much focus on the past, short-run bias, bias towards financial performance and information overload. The respondents did, on the other hand, not find the drawbacks posed any serious problem. Furthermore, the respondents did not find the performance measurement imprecise or open to manipulation. However, Kald and Nilsson argued that monitoring inside a company might not have the same need for structures that may be essential for reliable external reporting. The Nordic study found that measures were relatively well developed, and both financial and non-financial measures were combined and principally used for supporting decision-making. Heinrich (1999) found that US government bureaucrats in a job-training agency used performance-based contracting systems to make resource allocations. Service providers' performance relative to cost standards was the most important criteria in those decisions. On the other hand, performance standards were concluded to not have been well designed, as performance measures were not strongly correlated with program goals. She also suggested that implementation of performance standards in public bureaucracies is not the same as, and may be considerably more challenging than, implementation of such systems in private, profit-maximizing organizations. Thus, there are some possibly managerial implications of a public sector application of performance measurement as the BSC, which hitherto have not been given much consideration either in the scholarly or in the practitioner-oriented literature. Below I have elaborated on a justification for this statement. DiscussionI will here address some potential implications that should be given serious thought before one uncritically adopts the BSC in public management. Regarding managerial applications of performance measurement models such as the BSC, it seems as though the pragmatic alignment of organizational actions with shareholders' interest over time may be a major contribution to business management. The shareholders' strategy and hence the BSC will ultimately be tested through the market competition. When it comes to public management though, it may be wiser for the public manager to facilitate measurement by revealing the agents' strategies and agency efficiency rather than trying to align the performance indicators for the agents to the multiple public principals' ambiguous decisions. Strategic planning in firms is conceptually a close approximation to central planning in an economy. Central planning has traditionally been comprised of optimization of production with planning systems often utilizing multiple, linear equation systems, and distribution of income and products ideally judged by socially weighting each and every individual's utility (von Hayek, 1935). Schumpeter (1950) claimed in the preface to the second edition of his book Capitalism, Socialism and Democracy that "(we always plan too much and we always think too little". The BSC strategic planning system is deliberately made simple by its innovators, at least compared to alternative performance measurement systems developed for public management which are more congruent with welfare theory and agency theory (Mayston, 1985), and still more simple than "old fashioned" central planning theory. However, there is no single stakeholder with an unambiguous strategy decision in political institutions for public management to implement (though there could be less ambiguity in the administrative system in political institutions). That is precisely why we have political institutions. Political competition, together with common agency among other governance structures as rules and accountability, is a means for policy formation and implementation in modern, democratic and decentralized welfare states (March and Olsen, 1995). If the BSC is to be implemented in public organizations in the same manner as it is prescribed to be implemented in business firms, one may end up implementing a rigid, dysfunctional, Soviet-type, central planning system, rather than a flexible, decentralized learning system. This may pose a dilemma when using the balance scorecard in public management: If the BSC is used for aligning the ruling coalition's decisions with data on governmental performance, as the balance scorecard might be used for aligning a coherent stakeholder strategy with a firm's policies and actions in business, then revealing ambiguity is likely to result. If, on the other hand, one should try to facilitate the measurement of all the political stakeholders' different interests (which in fact might be useful for political negotiations and bargaining), then no coherent strategy would emerge but instead the performance measurement system would likely grow into a large, unmanageable and dysfunctional system. The performance of the agencies may be enhanced by letting the agents themselves select the performance indicators in the scorecard and monitor themselves and each other. Letting the agents align the performance indicators with their own strategies may enhance political competition for scarce resources in political institutions, which Breton (1996) termed intra, inter and extra governmental competition. This system could resemble market competition where instead of prices the performance indictors are carriers of essential information in decentralized decision making (von Hayek, 1945). This system could eventually have more managerial applications than a system assuming an explicit but non-existing, single stakeholder with clear intentions and unambiguous decisions and as if the main managerial problem is to operationalize the organizational goals. The proposed system instead emphasizes operationalization of agency efficiency and putting these performance indicators into a coherent and balanced framework. Thus, such a proposed system would lean more on the insights from positive agency theory and political economy as discussed above, while an unmodified BSC model would do less so. ConclusionsCan the BSC work in public management? My answer to this question is: probably yes. The BSC presents interesting options to widespread management problems as strategy and policy implementation and organizational control and accountability. In scholarly studies of the BSC it seems as though agency theory can provide much of the relevant theoretical perspective regarding business management. If the BSC is to be studied also in public management, then agency theory should be complemented with the public choice, bureaucracy theory branch of political economy. Performance measurement could also possibly be studied by evolutionary theory in order to appreciate dynamic change in complex structures and institutional change, rather than by agency theory only. It should be noted, though, that positive agency theory also appreciates uncertainty in its explanations of public bureaucracies. For instance, the legislature may abandon an agency altogether if the legislative anticipates that the agency uses information strategically and can not be monitored or governed efficiently. Nevertheless, for simplicity, one may come a long way in understanding how the BSC may work or not by using agency theory as the theoretical perspective of choice. I think the BSC has three main managerial applications. First, it is a versatile tool for developing, discussing and selecting the most decision relevant performance indicators in complex organizations as political institutions. Second, the BSC provides a practical approach to judge the basic premise in information economics: the benefit of information should exceed its costs. This could be achieved because the act of "balancing" the scorecard makes you think through carefully which performance indicator you want to discard and which you want to retain in the system. Even though only a few performance indictors for each of the four measurement areas are then left, these performance indicators may complement each other even though each of them individually is not perfect regarding validity and reliability. This procedure could therefore be very highly valuable both to managers and auditors because it reduces the number of performance indicators and the potential problem of proliferation and hence information overload. The third managerial application is educating busy stakeholders, managers and employees in management control in complex organizations. The BSC is a simple but practical performance measurement system in complex organizations despite, or rather precisely due to, challenging management theory issues. These three managerial applications, providing decision relevance, reducing performance indicator proliferation, and educating users, are, in my point of view, very important issues for implementing legitimate stakeholders' decisions in management. The BSC could have many important applications in public management as well as in business. However, uncritical adoption and implementation of the BSC in public management as it presently is prescribed for business strategy, could eventually turn out as reintroducing a Soviet-type, central planning model in political institutions. Such dysfunctions may evolve if one tries to measure strategic goals as if there were only one principal and unambiguous goals. This caution against uncritical use of the BSC, compared to seemingly less critique of performance measurement in general, may appear to be overly pessimistic on behalf of public management applications of the BSC. However, the BSC is building on, if not ancient, at least old and respected management models such as MBO. The BSC reminds us about two important aspects of strategy and management. First, the strategy of the firm or organization is the match between its internal capabilities and its external relationships (Kay, 1993). Hence, strategy implementation is balancing internal and external demands (Thompson, 1967; Pfeffer and Salancik, 1978). Second, management control and performance measurement are concerned with decision relevance (Mayston, 1985). Thus, the performance indicators on the scorecards must be useful for managers. These messages are no trivial contributions to business or to public management - almost regardless of how many times they have been said before. To avoid some of the potential managerial dysfunctions of the BSC in public management, a few lessons from agency theory and political economy may be useful. For instance, letting the agents monitor themselves and each other in political competition for scarce resources, could be a good idea after all. However, only positive studies extending over some longer period of time could really tell how applicable the BSC is for management compared to other performance measurement models. Note

Table I Generic management forms

Table II Prescribed applications and actual use of performance measurement |

||

|

Taken from Emerald Fulltext Website |

||