Monthly chart is currently congesting and RPTS expect market to be volatile in May or June. RPTS is looking forward to trading Volatility Breakout in Japan Raw Silk :-)

SPECIAL FEATURE 14/04/2005

Japan Raw Silk Futures on way to Volatility Breakout

Launched in 1951.

Exchange - Yokohama Commodity Exchange (Y-COM)

Web Site : http://host-a077.y-com.or.jp/renew/english/index_e.htm

Trading Methodology : Sessional Market

Trading Hours : 9.10AM, 11.00 AM, 1.10 PM, 3.00 PM (Japanese Time)

Contract Months : Six consecutive months from the current month

Last Trading Day : 3rd business day prior to the delivery day

Minimum Price Fluctuation : JPY 1 per kilogram

Contract Unit : 150 kg.

Brokerage Fee : RM 250.00

Tick Value : RM 4.80 (JPY 1 = RM 0.032)

Active Month : 6th Month

Liquidity - Very Low!

Initial margin - JPY 32,000 (RM 1,024 at JPY 1 = RM 0.032)

Current Development:

Japan Raw Silk Futures is characterized as low volume market. The sixth month is

most active market. When Raw Silk is getting more volatile, trading volume can

go above 500 contracts for the active month.

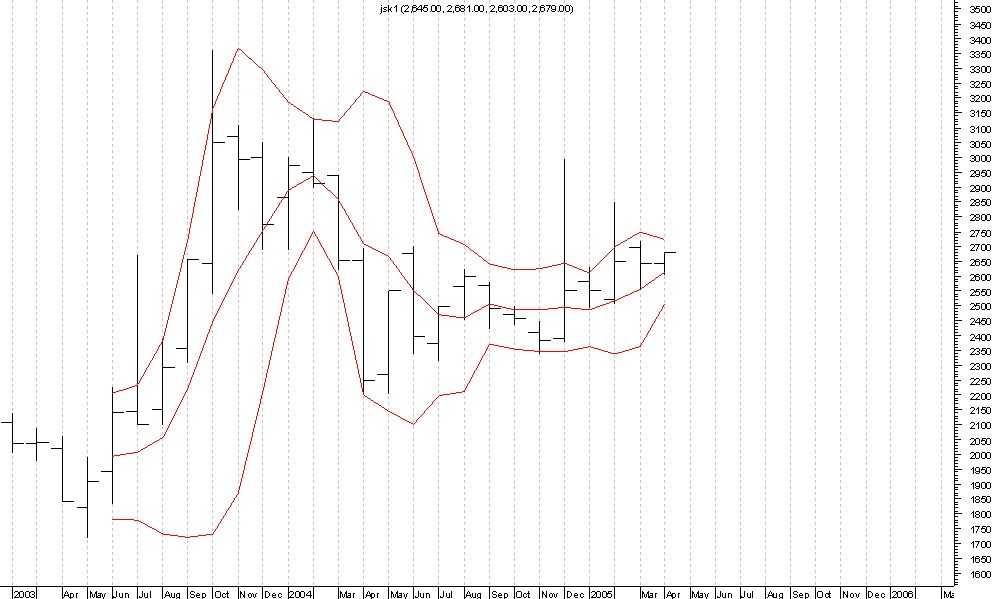

Monthly volatility breakout in the process:

Monthly chart is currently congesting and RPTS expect market to be volatile in

May or June. RPTS is looking forward to trading Volatility Breakout in Japan Raw

Silk :-)

For More Inquiries:

Our e-mail

: [email protected]