Background:

In Insurance-cum-investment accounts in Singapore, people have a choice of a suite of mutual funds ranging from low risk (bond funds and broad range) to very high risk (equity funds and narrow focus). Depending on their risk tolerance, they are allowed to choose any and to switch funds without penalty.

Each month, they will invest a fixed amount of money uptil a stated date in the future; probably 15 to 30 years depending on when they like to retire and the period of insurance validity. In reality, they can "top up" the money or sell their shares of the funds to withdraw the money at any time.

Dr Edna Chan of Singapore Polytechnic and I are working to develop a model with the above aim in mind. In such cases, we would like to find out what is the best strategy of buying and selling the units of the funds to maximize the returns at the end of the investment period. However the model and algorithm has to be simple enough that the ordinary investors can understand.

Assumptions:

At this time, we impose the following assumptions to simplify the problem. No transaction costs except for the difference in selling and buying price. This is true of the funds we are studying where we are allowed unlimited switching of funds.

Model:

Forecast Method:

Trend adjusted Simple Moving Averages

LP model:

Objective function - projected returns at the end of investment

Constraints -

overall risk of portfolio < risk tolerance

value of portfolio = invested amount + previous value

Iterative solution of LP model per month till the end of investment period.

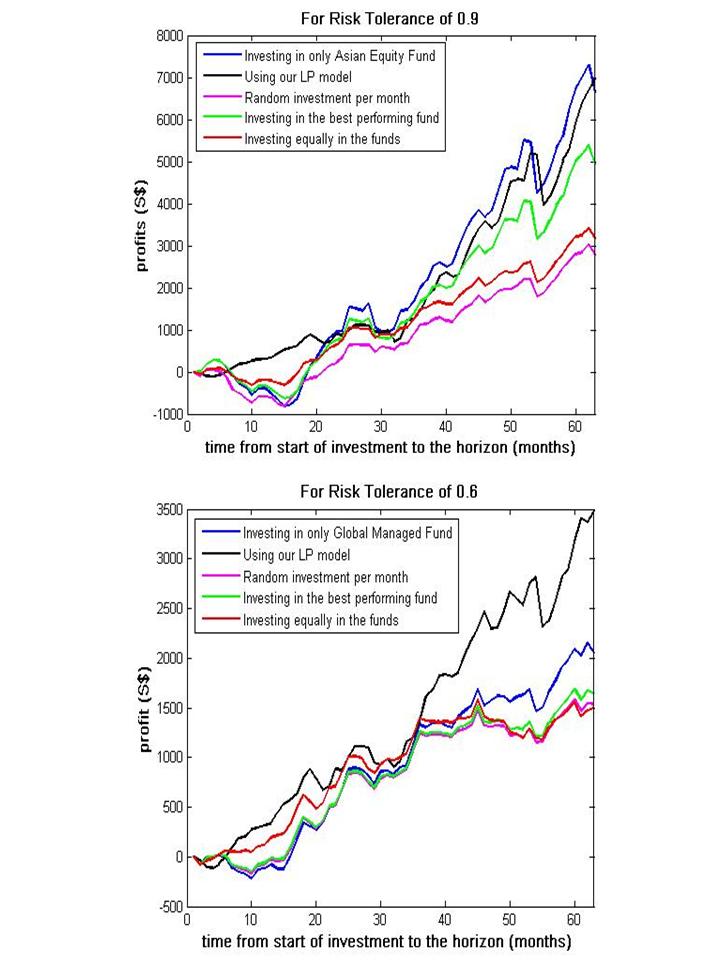

Results:

Tested our model using 4 funds provided by Prudential Singapore: Global Bond (risk ranking of 0.3), Global Equity (risk ranking of 0.8), Global Managed (risk ranking of 0.6) and Asian Equity (risk ranking of 0.9). Compare against 4 different ways of investment:

1. Fixed - choosing only one fund throughout and not switching (depending on the risk tolerance)

2. Balanced - dependent on risk tolerance, will invest in all funds with risk ranking less than the risk tolerance

3. Best - dependent on risk tolerance, will invest in the best performing fund at that particular month out of all funds with risk ranking less than the risk tolerance

4. Random - randomly chosen fund to be invested in out of all funds with risk ranking less than the risk tolerance

Not comparing with professional optimization models as the ordinary investor may not fully understand these models nor have any access to them. Our model and the above ways of investing are easily by those who have access to Excel spreadsheet. Below are our results for risk tolerances of 0.9 and 0.6 when we invest S$100 monthly and an initial S$3000.