Economy

Causes of the Great Depression

The Business Cycle

Annual Earnings from 1932-1934

Classical vs Keynesian Economics

The Bank Holiday and Emergency

Banking Act of 1933

Economic Differences

The Labor Force, 1929-1941

Welfare

The Bonus Army

Causes of the Great Depression

No one knows for sure what it was that caused the Great Depression,

although there are a variety of theories and events that may have played

a part. There are really two parts to the problem, those being (1)

why economic activity turned down, and (2) why having begun to go down

it continued to go down, and remain low for a decade.

The Federal Reserve indexes of industrial activity and factory production

reached a peak in June, 1929. It wasn't until October that other

indicators such as factory payroll, freight-car loadings, and department

store sales, were reported as being down. The economy then, had weakened

in the early summer (well before the crash). There are a variety

of explanations for this weakening. (1) More products were being

produced than were being consumed (supply outweighted demand). (2)

businesses misjudged the increase in demand, and acquired more inventories

than they needed. This resulted in less buying and a cutback in production

(an inventory recession) (3) more deap-seated factors: production

and productivity rose steadily per worker between 1919 and 1929 (output/worker

in manufacturing rising by about 43%). Wages, salaries, and prices

however all remained comparably stable (no comparable increase).

Since the cost of production fell, with prices staying the same, profits

increased. The profits kept the well-to-do spending, investing

in the stock market (encouraging boom), and encouraged a high level of

capital investment. The increasing investment in capital goods was

a principal device by which profits were spent. Anything that would

keep the investments from showing the necessary rate of increase could

cause trouble by decreasing consumer spending. So if investment failed

to keep up with the steady increase in profits, it would result in a

decrease in total demand (by falling orders and output) (4) It could have

had to do with the high interest rates, which finally caused people to

stop buying (5) Or trouble was transmitted to the economy because of a

weak sector such as agriculture (Galbraith 174-176).

The Federal Reserve indexes of industrial activity and factory production

reached a peak in June, 1929. It wasn't until October that other

indicators such as factory payroll, freight-car loadings, and department

store sales, were reported as being down. The economy then, had weakened

in the early summer (well before the crash). There are a variety

of explanations for this weakening. (1) More products were being

produced than were being consumed (supply outweighted demand). (2)

businesses misjudged the increase in demand, and acquired more inventories

than they needed. This resulted in less buying and a cutback in production

(an inventory recession) (3) more deap-seated factors: production

and productivity rose steadily per worker between 1919 and 1929 (output/worker

in manufacturing rising by about 43%). Wages, salaries, and prices

however all remained comparably stable (no comparable increase).

Since the cost of production fell, with prices staying the same, profits

increased. The profits kept the well-to-do spending, investing

in the stock market (encouraging boom), and encouraged a high level of

capital investment. The increasing investment in capital goods was

a principal device by which profits were spent. Anything that would

keep the investments from showing the necessary rate of increase could

cause trouble by decreasing consumer spending. So if investment failed

to keep up with the steady increase in profits, it would result in a

decrease in total demand (by falling orders and output) (4) It could have

had to do with the high interest rates, which finally caused people to

stop buying (5) Or trouble was transmitted to the economy because of a

weak sector such as agriculture (Galbraith 174-176).

There were a lot of things wrong, but here are some

primary weaknesses had a major effect on the ensuing disaster:

(1) Bad distribution of income. The rich were rich, and although

they only composed 5 % of the population, they had 1/3 of all personal

income. The proportion of personal income in the form of interest,

dividends, and rent of the well-to-do was twice as great as the years following

WWII. This meant that the economy was dependent on those with the

money to invest or spend a lot on luxury items, both of which are open

to fluctuations (much more so than the bread and rent outlays a workman

who makes $25 a week would have) (2) a severely depressed farm

economy (3) barriers to international trade in the form of high tariffs

(4) over production of consumer goods (5) The insufficient purchasing power

of working men and women (5) the slipshod practices of banks and credit

institutions (Twentieth Century... 21). There were a large

number of independent banks, so when a bank failed, it led to another bank

failure- the domino effect. (6) Bad corporate structure. Enterprise

in the twenties had not been conservative; it had an exceptional number

of grafters, promoters, swindlers, impostors, and frauds (Galbraith 177-183).

For More information see The

Crash and the Great Depression

Back to Top

The Business Cycle:

As any economist can tell you, looking at the market as a whole, there

is a business cycle involved. There are four phases to this cycle.

There is the peak, which is the top, then the downturn, then the trough

(the bottom), and the upturn, when total output begins to expand.

The nineteen twenties were in the upturn portion of the cycle due to a

boom in stock market prices, because of general optimism. Economists

and businessmen alike believed the fledgling Federal Reserve would stabilize

the economy, and that rapid technological advances would lead way to a

better quality of life and expanding markets. The business cycle

then hit its peak. The Federal Reserve had raised the interest rates

two times, once in 1928, and then again in 1929 to try to slow down the

economy, bringing on the initial recession (DeLong 1). The only place

to go was down, and the economy stayed down for more than 2 consecutive

quarters (called a recession). It continued to stay down and became

known as a depression. Looking at the graph below, 1932 was the worst

year of the depression, and could be considered the trough, the bottom

of the depression. Production and expansion then began to rise, in

part because of New Deal programs (Colander 489). By 1934,

conditions had improved to the point where, although 11,000,000 people

were still out of work, unemployment had decreased by about 1,700,000,

while the number of men and woman with jobs rose by close to 2,300,000.

The index of industrial production rose about six points, commodity prices

were up, as were stock market prices (Boardman 83).

Back to Top

Annual Earnings from 1932-1934

(Hard Times 26).

Airline pilot: $8,000.00

Airline stewardess: $1,500.00

Apartment house superintendent: $1,500.00

Bituminous coal miner: $723.00

Bus driver: $1,373.00

Chauffeur: $624.00

Civil service employee: $1,284.00

College teacher: $3,111.00

Construction worker: $907.00

Dentist: $2,391.00

Department-store model: $936.00

Doctor: $3,382.00

Dressmaker: $780.00

Electrical worker: $1,559.00

Engineer: $2,520.00

Fire chief (city of 30,000-50,000): $2,075.00

Hired farm hand: $216.00

Housemother--boys school: $780.00

Lawyer: $4,218.00

Live-in maid: $260.00

Mayor (city of 30,000-50,000): $2,317.00

Pharmaceutical salesman: $1,500.00

Police chief (city of 30,000-50,000): $2,636.00

Priest: $831.00

Public-school teacher: $1,227.00

Publicity agent: $1,800.00

Railroad conductor: $2,729.00

Railroad executive: $5,064.00

Registered nurse: $936.00

Secretary: $1,040.00

Statistician: $1,820.00

Steelworker: $422.87

Stenographer-bookkeeper: $936.00

Textile worker: $435.00

Typist: $624.00

United States Congressman: $8,663.00

Waitress: $520.00

Back to Top

Classical vs. Keynesian Economics:

Before the 1930s, economists had seen the market from a classical viewpoint

and only microeconomics were in existence. This began to change in

the thirties, with the help of John Maynard Keynes. When the US economy

fell into the Great Depression, businesses collapsed and unemployment rose

to the point where twenty-five percent of the workforce was out of work.

Previously, economics had concentrated on microeconomics (the study of

partial-equilibrium supply and demand). This did not take into account

the aggregate however, and so macroeconomics emerged (Macroeconomics is

the study of the aggregate moods in the economy, concentrating on problems

of growth, business cycles, unemployment, and inflation). There were

two groups of macroeconomists: Classicals and Keynesians (pronounced

KAIN-sian) both of which still exist today, although their differences

have become less distinct. Classicals were "macroeconomists who generally

favored laissez-faire or non activist policies" (Colander G-2). Keynesians

believed that the government should play an active role in the market (Colander

483-559).

Classicals argued that fluctuations in the market

were to be expected, that it would be strange if there were not fluctuations

when the market allowed individuals the freedom to do what they wanted

to do. Therefore, they should be accepted, just as people accept

the changes in seasons. If the government stepped in to take control

of the situation, people would anticipate the government's reaction, and

thereby undermine its attempt to control cycles. In reference to

unemployment, classicals believed that anyone who wanted to find work could

find work, at some wage, even if it was lower than a previous wage. If

a person was not working, it was his choice (making all unemployment frictional

- "unemployment caused by new entrants intoo the job market and people quitting

a job just long enough to look for and find another one" (Colander 493).

Economic growth was based on saving. If the economy wanted to grow,

people should save more, the more saving the better. Therefore, classicals

objected to government deficits (when gov't spends more than gets through

taxes). Classicals focused on the long run. While there might

have been problems in the short-run, in the long run the economy would

return to its potential output and natural rate of unemployment.

When the Depression hit, most Classical economists ignored the issue of

unemployment. When they were asked how the invisible hand could have

allowed the depression. They replied that the government policies

and labor unions kept prices and wages from falling, not allowing the invisible

hand to coordinate economic activity (Colander 483- 559).

Keynesians on the other hand, felt that fluctuations

were symptoms of underlying problems in the economy, and that the government

should step in and deal with them. They felt the same way about unemployment-

Society owes people jobs that equal their training or job experience.

Furthermore, jobs should be close enough to home that people don't have

to move. This would mean most employment was structural "unemployment

caused by economic restructuring making some skills obsolete" and cyclical

"unemployment resulting from fluctuations in economic activity" (Colander

492). If people weren't working and they wanted to, Keynesians wanted

a short run policy to address this. During the depression, people

became dissatisfied with Classical economists "have faith" solution and

wanted help at that moment. As Keynes said, '"In the long run, we're

all dead"' (Colander 558). Keynes concentrated on the the causes

of the Depression, and on solutions to it. He believed that wages

and the price level adjusted to changes in expenditures, and it could get

stuck in a rut. If people stopped buying, then production would decrease,

causing people to lose their jobs. Those people would then have less

money and would save more and buy less, going around in a circle, until

the economy was stuck at a low level of income. Through this thought

process, Keynes created the theoretical foundation that unemployment was

caused by too little spending (Colander 483-559).

Back to Top

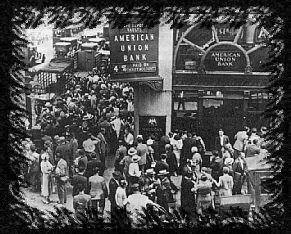

The Bank Holiday and Emergency

Banking Act of 1933

On Monday, March 6, 1933 the president along with his economic advisors

decided to close every bank in the country. By the third month of

1933, over 4,000 banks had gone under. Governors from 47 states had

already declared bank holidays in order to stop the frantic withdrawals.

Roosevelt's announcement however, put a halt to all banking transactions

anywhere not specifically authorized by the secretary of the treasury and

the president. It also outlawed the export of gold, in an effort

to keep reserves from being further depleted. The bank holiday was

a short term solution which could remain effective only until Congress

acted. Both houses approved Roosevelt's administration-drafted Emergency

Bank Act on Thursday, March 9 (Watkins 150-151). The Emergency Bank

Act

not only authorized the president to do what he

already had done--close the banks and embargo gold--but stipulated that

no bank could be reopened until approved by the

secretary of the treasury, permitted the comptroller of the currency to

install conservators over insolvent banks and gave

such conservators the power to reorganize them, authorized the purchase

of bank stocks and notes by the Reconstruction Finance

Corporation to provide qualified banks with long-term investment

funds, gave the president greater control over credit,

currency, foreign exchange, and the setting of the price for gold and

silver, and allowed the Department of the Treasury

to call in all privately held gold and gold certificates to be exchanged

for

paper currency (Watkins 151).

Back to Top

Economic Differences:

In 1933, at the London Economic Conference in June, the United States

announced that it would be coming off the international gold standard as

a way to measure the worth of American currency. The Gold standard

meant that currency would be measured in terms of a fixed amount of gold.

Instead, the American dollar would measure its worth in relation to other

countries currencies depending on the demand for it in world markets, as

Great Britain had been doing since 1931. By announcing this decision,

Roosevelt was actually encouraging a currency war. Though Roosevelt

continued to support the purpose of the economics conferences, his administration

was divided. Cordell Hull, the secretary of state, was a stout internationalist.

He believed that by lowering trade barriers in the form of protective tariffs,

the world's economy problems would be saved. One of Roosevelts closest

friends however, assistant secretary of state Raymond Moley, was less convinced

with the international approach. He believed that national solutions

should solve national problems. On July 3rd, Roosevelt gave the "Indianapolis

Statement", which sunk the ideas of Hull and the conference. "From

the deck of the cruiser Indianapolis the president announced his

own opposition to the very idea of stabilized currencies and pressing upon

Europeans that need for balanced budgets and domestic financial reforms"

(Depression America 48). By taking itself out of the international

gold standard, Roosevelt felt that America's exports would be given a boost.

The lowered value of the dollar would lower the cost of exports to foreign

buyers. Roosevelt also felt that that a currency-stabilization scheme

might ruin his New Deal efforts to raise prices, particularly farm prices.

Therefore, Roosevelt and Moley went with the nationalist approach, forming

the Johnson Act of 1934 (chief creator Senator Hiram Johnson of CA).

This act barred foreign governments who had not paid back war debts from

floating loans on the American financial markets (Depression America 47-48).

Back to Top

The Labor Force, 1929-1941

(Gregory 84)

|

Year

|

Total Labor Force #

|

Total Labor Force Noninstitutional Population *

|

Armed Forces

|

Civilian Labor Force

|

Employed

Total

|

Employed Farm

|

Employed Nonfarm

|

| 1929 |

48,017 |

55.1 |

260 |

47.757 |

46,207 |

10,541 |

35,666 |

| 1930 |

48,783 |

55.0 |

260 |

48,523 |

44,183 |

10,340 |

33,843 |

| 1931 |

49,585 |

55.2 |

260 |

49,325 |

41,305 |

10,240 |

31,065 |

| 1932 |

50,348 |

55.4 |

250 |

50,098 |

38,038 |

10,120 |

27,918 |

| 1933 |

51,132 |

55.6 |

250 |

50,882 |

38,052 |

10,090 |

27,962 |

| 1934 |

51,910 |

55.7 |

260 |

51,650 |

40,310 |

9,990 |

30,320 |

| 1935 |

52,553 |

55.6 |

270 |

52,283 |

41,673 |

10,110 |

31,563 |

| 1936 |

53,319 |

55.7 |

300 |

53,019 |

43,989 |

10,090 |

33,899 |

| 1937 |

54,088 |

55.9 |

320 |

53,768 |

46,068 |

10,000 |

36,068 |

| 1938 |

54,872 |

56.0 |

340 |

54,532 |

44,142 |

9,840 |

34,302 |

| 1939 |

55,588 |

56.0 |

370 |

55,218 |

45,728 |

9,710 |

36,028 |

| 1940 |

56,180 |

56.0 |

540 |

55,640 |

47,520 |

9,540 |

37,980 |

| 1941 |

57,530 |

56.7 |

1,620 |

55,910 |

50,350 |

9,100 |

41,250 |

* means entire population excluding people under 14, students, wives

and mothers at home--who were not counted as part of the work force, and

those who were institutionalized.

(Source: Wattenberg, Statistical History, 126)

Back to Top

Welfare

Before the Roosevelt administration, most relief

services were provided by voluntary charities. The Hoover administration

especially had declared that it was not the place of the government to

provide such services to its people. To combat unemployment, President

Herbert Hoover established the President's Emergency Committee on Employment

(PECE) in 1930. It was later renamed the President's Organization

on Unemployment Relief (POUR). Its sole purpose was to urge business

to rehire workers and to create a sense of moral support and direction

world-wide. But by 1931, voluntary agencies across the nation "tottered

under the weight of rising case loads" (Gerdes 127).

Thus, in 1933, when the Roosevelt administration

established the Federal Emergency Relief Administration (FERA), people

were shocked. It was considered "a landmark in American social welfare

history" (Gerdes 125-6). It was the belief of Roosevelt and his advisors

that the economic crisis had created such high levels of joblessness and

poverty that it had become impossible for the government to ignore.

These crises, it was believed, could undermine the fabric of American culture.

Federal action, therefore, was needed to preserve the "American way of

life" (Gerdes 126). Furthermore, the administration believed,

it was necessary to establish a series of work relief programs would need

to be enacted. This assertion led to the establishment of the New Deal

works projects.

Additionally, in 1933, Americans were able to insure

themselves against hospital care cost for the first time through a nonprofit

system called the Blue Cross. Before long, millions of people were

covered by this insurance (Boardman 82).

Back to Top

The Bonus Army

At the peak of the depression, 1932, thousands of WWI veterans

paid a call to Washington, ordering Congress to pay them a wartime bonus

which was scheduled to be paid in 1945 immediately. This movement

was led by Walter Waters, a former medic for the 146th Field Artillery. The group rose to over twenty-five

thousand within two months, and Hoovervilles began to spring up all around

Washington and in abandoned buildings. Representative Edward Eslick

spoke before colleagues to support the veterans. During a debate

over a bill which would allot some of the bonus money to the veterans,

Eslick died of a heart attack. The next day, the bill was passed

by the House, 21 to 176 with 40 abstaining. It then went on to the

Senate, where it was defeated 62 to 18, with the help of Hoover.

(Hoover was against increasing the national debt and a heard protester

of the bill.) Crushed, many families left for home. Hoover

even encouraged a 100,000 dollar transportation loan bill which would help

marchers to return to their homes. Some families decided to stay

however, hoping the situation would improve. Fearing health problems,

Hoover ordered U.S. troops to escort anyone who remained out of the city.

Army chief of staff Douglas MacArthur went a little further, by burning

the shantytowns and routing any remaining campers with water hoses, bayonets,

and tear gas (Nishi 14-17).

medic for the 146th Field Artillery. The group rose to over twenty-five

thousand within two months, and Hoovervilles began to spring up all around

Washington and in abandoned buildings. Representative Edward Eslick

spoke before colleagues to support the veterans. During a debate

over a bill which would allot some of the bonus money to the veterans,

Eslick died of a heart attack. The next day, the bill was passed

by the House, 21 to 176 with 40 abstaining. It then went on to the

Senate, where it was defeated 62 to 18, with the help of Hoover.

(Hoover was against increasing the national debt and a heard protester

of the bill.) Crushed, many families left for home. Hoover

even encouraged a 100,000 dollar transportation loan bill which would help

marchers to return to their homes. Some families decided to stay

however, hoping the situation would improve. Fearing health problems,

Hoover ordered U.S. troops to escort anyone who remained out of the city.

Army chief of staff Douglas MacArthur went a little further, by burning

the shantytowns and routing any remaining campers with water hoses, bayonets,

and tear gas (Nishi 14-17).

Back to Top

Return

To Home