Now that we have seen that a change in our perception of economics is needed, it is time to consider what should be done to implement these changes. Any change, particularly change as significant as the Three Steps to Economic Freedom, involves disruptions. Our task now is to examine the potential disruptions and find methods that will minimize any adverse effects. We will address each of the steps in the order they have been presented.

First is the change from uncertain future money value to a stable currency. Because the future value of money is now uncertain, extraordinary measures need not be considered for the transition. That is, as things now stand the future value of money may be anything, including the same value as today. Therefore, making certain it is the same as today imposes no unfair hardship on anyone who guessed it would not be the same. There are, however, some implications of the change that would be useful to acknowledge and others that will help to establish a starting place for the transition.

The major effect resulting from a stable currency is lower money interest rates because of the elimination of any need for an inflation premium. The most significant effect would be on long term rates. This means existing contracts for long term borrowing must be either renegotiated or refinanced to bring these contracts into conformance with the lowered lending risk.

There are some bonds, particularly government issues, that have non-callable features that prevent refinancing. These features were offered to obtain lower interest rates than would have been available without these provisions and these borrowers have, therefore, already been compensated. It would, however, be prudent for anyone contemplating borrowing long term in today's market to consider that future rates will be significantly lower and insist on provisions to renegotiate or refinance any new commitments made based on uncertainty of the future value of money.

The other consideration to be examined is the method of implementing the change. The method of controlling money value is what it has been since creation of the Federal Reserve System. It is control of credit availability through Federal Reserve System open market operations. The only distinction is the measure used to determine the actions to be taken.

During the development of the evidence that there is no significant lag between Federal Reserve open market activity it was shown that a predicted estimate of how much government debt the Federal Reserve should buy from or sell to the open market. But as was also noted, the statistical correlation used to demonstrate this was and is just a correlation and can not be relied upon once the method is implemented because the very knowledge of the method will affect the behavior of people. Therefore, it becomes necessary to simply adjust the purchase/sale decisions based on actual outcomes of those choices.

Monetary Trends, a publication of the St. Louis Federal Reserve Bank lists the amount of government debt held by Federal Reserve Banks. Changes in the amount of government debt held by the Federal Reserve System is the net effect of the FED's open market activities. Over the four year period ending June 1988 the net result of these activities was a $74.3 billion increase. This period is approximately 1,000 working days -- 4 years at 52 weeks per year, 5 working days per week less 10 holidays per year gives 1,000 working days total -- therefore the average net activities over this period have been $74.3 million per working day.

While it can be said that inflation has been low recently, it has not been low compared historically and is certainly not the zero rate that is desired. Therefore, the new policy should start with something less than this, say $50 million per day. And, because the effect is now recognized, there is no need to make the many buy-sell machinations now done to disguise the FED's activities and, not insignificantly, increase the expense of these operations.

The actual amount needed will, of course, vary with economic activity and must be redetermined every time the value of money differs from the established standard. The method of determining the amount is similar to the method to be used for determining the monopoly tax. The only difference is that here we are not interested in causing money value to grow, rather, we are interested in stabilizing its value. Therefore, adjustments in open market purchases can be made every month based on the value of the Consumer Price Index instead of every other month based on a growth rate as with the monopoly tax. A minor consideration applicable only during the transition period is the low frequency of measurement of the Consumer Price Index.

Until it becomes believable that money value will be held constant a more frequent measure of the value of money may be desirable. Accurate measurement of the value of money involves substantial corrections for changes in the availability and quality of products, changes in consumer tastes and seasonal preferences for many products. Such measurements take a considerable effort to make and are concerned with longer term product changes. A less accurate measure of money value can be done weekly or even daily by omitting these factors.

Next we will look at Step 2 - Taxing Monopoly. Many effects of this tax have already been detailed in the presentation of the tax itself and the widget model. However, some speculative notes about what responses can be expected as a result of this change are in order.

First, and perhaps most significant, is the response that can be expected from corporations. Throughout American history there have been numerous times that legislation has been threatened or enacted to control the excesses of monopoly. It has long been recognized that these excesses are detrimental to the economic well-being of both individuals and the nation as a whole.

With the monopoly tax in place, it is reasonable to expect that these companies will reorganize themselves into companies of smaller size and singular businesses. Particularly, wholly owned subsidiaries would be spun off to stockholders as independent companies. Similar changes -- creation and spin-off of subsidiaries -- would substantially increase competition. This is because with monopoly profits taken as taxes they will no longer be able to exploit their customers by price gouging and must earn their keep by producing better products at lower prices. They can do this only by keeping their companies lean to avoid the higher tax rates for large companies. Such reactions to the tax system would likely be sufficient to accomplish the desired ends of monopoly legislation without all the court fuss and expense attendant to legislative attempts to attain these goals.

If a large size is required for any particular company it will be because its size generates economies of scale and does not simply provide an opportunity to exploit the marketplace. Because we cannot be certain what the appropriate sizes of companies will be some adjustment in the tax brackets will undoubtedly be required.

If the relevant size becomes much smaller as would be evidenced by a very high tax rate for the lowest tax bracket then it would be necessary to lower the minimum tax bracket from the suggested level of $100 million in assets. Conversely, if it becomes apparent that companies as small as $100 million in assets are insignificant because tax revenues from these companies become too little, then the minimum tax bracket would, of course, be raised. Speculation of which effect will predominate is beyond my vision though my suspicion is that the breakup of much of the present conglomeration of unrelated businesses into one corporation would significantly reduce the size of the lowest tax bracket.

Another consideration of the tax brackets concerns the increments. It cannot be determined without actual experience how large the increments should be but the method to redetermine the increments is recognizable. That method is to observe the tax rates for each bracket as they develop over time. If the tax rate for a given increment becomes small relative to other rates then it is appropriate to eliminate that increment. If, on the other hand, the tax rate becomes large compared to the others then it is appropriate to create a new tax bracket between it and the bracket immediately above or below it. Again, I have no realistic way of knowing whether one or many such brackets will result but, because of the progressive nature of monopoly significance, I suspect it will be more than one.

The next relevant response to the monopoly tax is the effects of transition away from the present tax system. It would do little, if any, harm to leave the corporate income tax [NOTE: The corporate income tax is a non-distortionary tax -- i.e., it does not distort the point of maximum profit -- tax.] in place while determination of the best rates of the monopoly tax proceed. That is, the monopoly tax would start small and grow towards its optimum rate. Allowing the monopoly tax to be a credit towards the corporate income tax would allow this transition to be completed with no adverse effects. Once the corporate income tax is overcome entirely by the monopoly tax, it can be repealed as unnecessary. The same can not be said for the personal income tax.

There are two major problems with a transition from the personal income tax system to the monopoly tax system. First, it is reduction of manufacturing cost (realized in the widget model by the abolition of personal income taxes) that propel the benefits of economies of scale. Second is the personal income tax system itself.

Over the years there have been many objections to the personal income tax system. The system has been and is being resisted by freedom lovers who call themselves patriots but whom the Internal Revenue Service labels protesters or shirkers. The patriots battle may appear to have culminated this year with passage of the "taxpayer's bill of rights." But, in fact, this bill is not what will be the real outcome of the patriots continuing battle with the American Gestapo (i.e. -- Internal Revenue Service). The real outcome is only now being spread among the patriot community.

The real outcome of the patriots struggle is the discovery that personal income taxes are not authorized by the sixteenth amendment as is taught in our government schools. The sixteenth amendment did no such thing. From the Supreme Court came these words of the nature of the sixteenth amendment. The court said it:

Taxpayers need a special "bill of rights" because as taxpayers they have admitted to the crime of being taxpayers. They had no trial, did not even know it is a crime. But, unlike people accused of murder, rape, robbery or some other heinous crime, they do not have the protection of the true "Bill of Rights" -- the one in the Constitution -- because they have already confessed to their "crime" of being taxpayers. All that is to be resolved is the penalty -- the amount of tax and/or fines to be paid.

Taxpayers are assumed by our corrupted courts to be convicted of being taxpayers without ever inquiring if they are in fact so situated. Like other convicts, they are assumed to not be entitled to the full protection of the Constitution. But, they are not really vicious people and do deserve some protection from the Gestapo. That is why they need a special "taxpayer's bill of rights." As more and more people learn of this discovery, the personal income tax system with all its convolutions and complications will fall of its own weight. [A compete discussion of this issue is available in books circulated among patriots. My favorite is The Best Kept Secret -- Taxpayer v. Non-taxpayer, Otto Skinner, Dept F-2, P.O. Box 6609, San Pedro Ca., 90734.]

The relationship this has to the transition from the personal income tax system to the monopoly tax system is that as this becomes known there will be no opportunity to phase out the personal income tax as the monopoly tax is phased in. It is obvious, however slow they may be to respond to changes, that wage rates are NOT independent of the personal income, social security, and unemployment taxes that substantially increase production (variable) costs as presently imposed.

Wages, like all other prices, are negotiated through market forces. The actual wages settled upon take into account all the associated liabilities of both sides of the negotiations involved. That is, wage demands reflect the reality of the tax, travel and incidental costs of employment as do wage offers reflect all the expenses of health and retirement benefits, payroll and social security taxes, etc. Changes to which all take time to filter through to negotiated outcomes of nominal wage rates.

To avoid this difficulty -- although it would probably be less disruptive if the tax could be gradually transitioned -- I suggest we be done with it and simply abolish the tax immediately and declare a moratorium period of six months to adjust personal service (wage and salary) contracts that have assumed the existence of the personal income tax system.

There is a related item concerning the potential effect of the monopoly tax on money interest (not economic interest/normal profit) rates. That is the effect on the cost of funds at banks and other lending institutions. If bank deposits -- assets to depositors but liabilities to the institutions -- were to be included in the tax base like other debt obligations of corporations then this would cause the cost of funds and money interest rates to become prohibitive. To avoid this singular problem, these institutional liabilities -- any deposits insured by FDIC or FSLIC or otherwise qualified except by the limitation as to amount of coverage -- would be excluded from the taxable value of these institutions.

One last consideration of the monopoly tax and the equation of exchange value is that we have only addressed federal government revenues. The currently favored proposal for state and local taxation among Georgists -- people who are familiar with the writings of Henry George -- is to separate the tax on land -- the site value -- from the value of improvements -- buildings, etc. -- and tax land at a higher rate than improvements.

While it is true this proposal does improve the social condition over the present tax system, application of the monopoly tax system to state and local taxes does even better. With the Equation of Exchange Value to determine the best tax rate and a homestead exemption for people to live freely in their home of a reasonable value, the tax system will not only cause more efficient use of vacant or underutilized land it will also prevent monopoly abuse of appropriately developed property.

Application of the monopoly tax to finance state and local government requires a few minor changes to reflect the different tax base and the different level of value that is relevant. The tax base for state and local government is the value of real estate that is monopolized.

Because the monopoly effect of land occurs with small parcels the tax brackets and tax rates are for each $100,000 increment of value above a homestead of $100,000 and $1 per month per $1,000 of value. The rate change procedure is the same as with the corporate tax. That is, the initial rate is tried, the rate is increased $0.02, growth rates in tax revenue are compared and then all further changes are based on growth rate of revenue. However, a different assessment method is needed.

Because the value of most corporations is determined in a substantially liquid market there is no need to establish a value assessment process. For individually held property we need to do so. The assessment process requires that a condition be set on the ownership of taxable property. That condition is that anyone can buy the property at the owner's value assessment.

The assessment can be changed by the owner at any time but:

Because, like the corporate monopoly tax, the tax grows at its optimum rate, the tax rate should not be decreased when the revenue exceeds government needs. Any excess should therefore be used first to remove other (distortionary) taxes; next to reduce any state or local debt; and, the rest could either be held for emergencies or returned to citizens as a junior version of the Citizen's Dividend.

This assessment procedure will not be required for most corporations but, for those few that are individually owned and large enough to be subject to the tax, the self assessment procedure can be used for the same reasons that they are used with the real estate tax. That is, privately held corporations can be required to state their market value and be subject to purchase by anyone who wants the business.

Lastly we will examine the implications of Step 3 - The Citizen's Dividend. It is with some reluctance that I present speculations on this effect. It is not that I feel less confident of these speculations than the others already presented. It is simply that in our world of cognitive dissonance the implications are so hard to believe. The wonderful world of widgets takes us to a realization that we have been living on the wrong side of the looking glass. But, this is where they lead, so this is where this argument shall go.

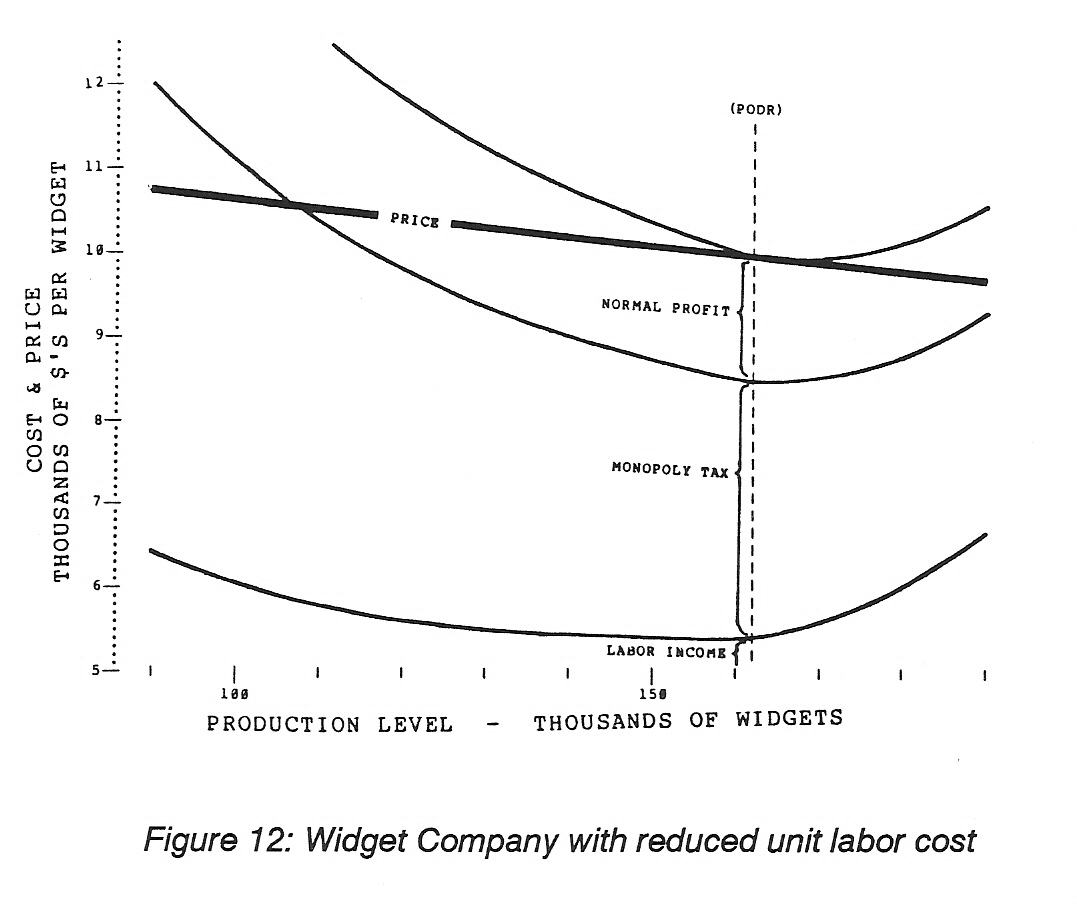

We will start by using the model widget factory one more time with lower unit labor costs to show that it is unit labor costs that are the second -- after excessive monopoly profits -- cause of restraints to production. Because workers standard of living relates to the net (after tax) income they receive and it is their standard of living that is the essential point of their wage demands, the elimination of their tax liabilities plus the distribution of the Citizens Dividend will undoubtedly lead to a lowering of wage demands with the consequent reduction in production (variable) costs and attendant reduction in prices, etc.

For our example we will lower these costs by 10% to $5,400 for production at the physical point of diminishing returns. No other change to costs is made and, as can be seen in Figure 12 and Table 5, after all the iterations of investment, tax adjustments and Citizen's Dividend increases the point of economic diminishing returns has risen to 162,000 widgets with all its associated increases in labor income, tax revenue and normal profit. Further reductions in labor costs will, of course, result in similar increases in the level of production.

We can now answer the question presented in the Prologue - Cause and Effect: What is it that impedes, limits or governs our ability to divide the labor of production into the pleasures of production?

The limit is our ability to be economically free. So long as we have no real concern over our economic well-being we will not have to deny people opportunities by minimum wage laws, trade barriers, work rules that say a plumber can't change a light bulb and corporations that protect their investments by withholding more efficient or effective tools and products until they recover their present investment. There will, of course, still be those tasks that no one wants to do because they are too dangerous or otherwise disagreeable. These jobs will always require some pay to get done. But, that is a far cry from the way things are now. And, because it is unit labor costs that are of concern it is quite probable that removal of all the featherbedding and foolish work rules that do nothing but decrease efficiency and the cessation of withholding labor saving inventions to supposedly save jobs will, in fact, allow higher wages than presently exist.

This may not be convincing in its totality but, it is all I intend to say on the matter now. Next it is necessary to address how the Citizen's Dividend is to be determined. The basic measure suggested for this purpose is the measure of Gross National Product. That is, by using the methodology of the monopoly tax and the growth rate of Gross National Product to determine increases or decrease in the Citizen's Dividend it will grow sufficiently large to set people free to chose their jobs, their educational pursuits, etc. but not so large as to allow desire for idle pursuits to waste productive time and cause production to decline.

The Gross National Product, unlike the Consumer Price Index used for the monopoly tax adjustment, is measured only quarterly so the adjustments in the amount of the dividend would be only every six months. To avoid excessive burden on the Federal Reserve System's task of controlling money value, I suggest that a modest start, say $50 per quarter per resident adult citizen, would be enough to determine what the dividend should be.

The Citizen's Dividend would also affect the level of wages that are necessary for a decent living. That is, as the dividend becomes greater the demand for higher wages will be lessened and that, in turn, will increase the economic points of diminishing returns.

Other items affected by the Citizen's Dividend include the current problem of distinguishing economic emigration from political asylum. With nominal wages reduced, there would be less economic incentive to emigrate to the United States and the problem could well disappear. The effect on the propensity to crime among the economically deprived can only be to reduce this propensity. The effect the Three Steps to Economic Freedom would have on world affairs, particularly after other countries adopt the process, would verge on the unimaginable. Without economic incentive to fight wars, how many fewer of them would there be?

Where this process will ultimately lead is anybody's guess. For

me I can say only that - I