Perhaps this is too obvious to satisfy economists' penchant for complexity. But, for whatever the excuse, this tautological certainty remains a tautological certainty.

Actually, economists are not totally oblivious to the effect of monetary policy on prices. It is just they have great difficulty in defining what money is. In their search for a definition of money they have found a good correlation between what they choose to call money and the Consumer Price Index.

Economists have found they get their best correlation with a two to three year time lag between the measure of money supply and the Consumer Price Index. Because the level of economic activity two or three years in the future can not be known, this apparent time lag in the response of prices to their measure of money supply has led them to the conclusion that the value of money can not be directly controlled. They dress up this conclusion in circumlocutious nonsense they call economic analysis, but that is the essence of their conclusion. The truth is quite different.

One error economists make in their analysis is inconsistent use of their definitions of money. For example, economists have defined several measures of money supply that they call M1, M2, M3, etc. To obtain the definition they call M1 they add together four measures of items people use in conducting their financial affairs:

They assume that all these components have the same effect on prices and perform their correlations with only one constant. The actuality is that each component has a different effect on money value and there should be as many correlation constants as there are components.

One must suspect economists cling to their assumption that only one constant is needed because they found this correlation before the advent of cheap computers. Without the use of computers the calculation of correlation constants is very tedious. The more constants to be found the greater the tedium. This seems a reasonable excuse for the early researchers who discovered this correlation but it is difficult to sympathize with today's experts who continue to cling to this foolishness.

I have not performed any correlations correcting only this particular error. For now let it be sufficient to state that elimination of the economists' assumption that only one constant is needed will both improve the correlation and reduce the arbitrary time lag they use to overcome their assumption. With the equations I will introduce later the correlation is almost perfect and there is no time lag.

The next error seems to arise from confusion between controlling the quantity of money and controlling the value of money. There is great reluctance to accept that what is defined as money does not matter when searching for the method to control the value of money. For that matter, money need not even be defined. All that is needed is a method to control its value and a measure to determine the amount of control to be applied.

We have no difficulty in distinguishing between two such diverse things as war and oil. We also have little difficulty understanding that war significantly affects the price of oil. The relative value of oil is changed because the quantity of oil available becomes less while the quantity of other things is not changed. The economic value of all things, including money, are affected by relative availability.

The method to control the value of money is through central bank open market operations. Many observers recognize central bank open market operations as the method of controlling the quantity of money. This, of course, depends on one's definition of money. If the definition includes demand deposits as a component then the quantity of money is directly affected by open market operations. If these deposits are called substitute money then the money supply is not directly affected. But, in either case, open market operations do affect the value of money.

When a central bank buys securities from the open market it does so by creating a demand deposit to the credit of the seller. When it sells securities it does the opposite. Creation or extinction of demand deposits changes the availability of money or money substitutes without changing the supply of products and services available for purchase. Like all changes in supply, open market operations affect the value of money. The critical question is -- How much should the central bank buy or sell in the open market?

Much of the circumlocutious nonsense that is presented as economic analysis deals with this question. Many economists say monetary policy should attempt to maintain a constant growth rate in one or another of the various measures of money supply. Others say the central bank should conduct its open market operations to control interest rates. But, in today's world of arrogant certainty, most economists seem to believe that monetary policy should be determined by a presumed relationship between money supply and some measure of economic activity or unemployment.

The arguments in favor of a constant growth rate of the money supply are based on the quantity theory of money and a presumed lag in the response of prices to changes in the supply of money. The quantity theory of money is simply the tautological statement of the supply-demand relationship among all economic goods and services. The presumed time lag is an assumption that the specific correlations discussed earlier are proof of an economic law. The universally recognized truth that correlations do not differentiate among cause, effect or circumstance is ignored in the rush to make hay of these correlations.

The major monetary policy tool is central bank open market operations. Because open market operations create or extinguish demand deposits, a component of all of the measures of money supply, these actions directly affect these measures. However, after deposits are created or destroyed, individuals realign the type of deposits they hold and banks realign their loans and other investments to accommodate the requirements of legal reserves banks must maintain to avoid restrictive regulations. Each type of deposit, loan and investment has a different effect on the measures of money supply.

Because of uncertainty in which choices will be made, the central bank can only estimate the particular amount of securities to buy or sell in order to meet its target for money supply. That is, the central bank must buy or sell securities and then wait to see what happens to the measure of money supply the bank is trying to control. Based on whatever happens to that measure it must then estimate what to do next. A rather clumsy process at best.

Attempts to control interest rates by monetary policy are based on more tenuous arguments than the process to control the supply of money. When a central bank buys bonds from the market the added demand for bonds causes the price of these bonds to increase. An increase in the price of a bond is the same as a decrease in its interest rate. Thus, an increase in open market purchases appears to cause a decrease in interest rates. But, like so many other shallow analyses that omit pertinent factors, this process fails in practice.

Purchase of bonds by the central bank increases the demand for bonds. It also increases the supply of money. This additional supply reduces the value of money and the falling value of money in turn increases inflationary expectations. These effects then cause an increase in interest rates. To try to reduce or maintain interest rates by monetary policy the central bank must buy bonds at ever increasing rates to keep ahead of the increase caused by inflation and inflationary expectations. Eventually the market anticipates the actions of the central bank and both demands and accepts higher interest rates than may be indicated by the current rate of inflation. This vicious cycle continues until a brave central banker reverses the cycle and sells bonds to raise interest rates and reduce inflation. This leads to lower interest rates until another economic genius convinces the monetary authority it must buy bonds to reduce interest rates!

The arguments claiming that monetary policy is an effective tool to manage economic activity are the most difficult to refute. The difficulty is not that the arguments of these claimants are so strong. It is that there are no rational arguments used to demonstrate these claims. There is only blind faith and the nonsense called "income analysis" or some equally obfuscatory argument. Psychologists have a term for this phenomenon. They call it "cognitive dissonance." It refers to the behavior of people who simply refuse to admit any evidence that does not affirm their beliefs. There have, however, been arguable points that have given rise to this cognitive dissonance. These include such things as the famous "Phillips-curve" and John Maynard Keynes "propensity" arguments.

The Phillips curve, a correlation purporting to show a trade-off between unemployment and inflation, has long been so discombobulated that only the most obstinate zealots attempt to demonstrate this relationship now. They just refer to the coincidence observed by Phillips and accept their beliefs despite any contrary evidence.

Occasionally these economic experts will argue that the Phillips curve has become discombobulated because of a shift from "demand-pull" to "cost-push" inflation. They then assert that the relationship between inflation and unemployment shifts up or down depending on the ludicrous notion that there are these two types of inflation. The obvious truth that the only difference between demand-pull and cost-push is which side, buyer or seller, of a transaction is describing a price increase is glossed over in self-righteous declaration that the Phillips curve is a viable economic relationship. However, in all their arguments before and after the Phillips curve became discombobulated, they have never shown any rationale or evidence that explains a causal relationship between inflation and unemployment. They do not show such evidence because there is none. There is only the historical coincidence observed by Phillips and their own blind faith.

The arguments of Keynes are so involved that no one quite understands these arguments. So, the belief persists with the support of some economic experts followed by people disenchanted with the current opposition.

The propensity arguments of Keynes were based on observed differences between rich and poor. Because the rich have more than they need they are said to have a "propensity to save." The poor on the other hand have a "propensity to consume." Keynes argued that transferring money from those with a propensity to save to people with a propensity to consume will cause an increase in economic activity. As disturbing as this is to my conservative nature, I must admit that this argument is actually valid. The problem arises with the methods used to implement the process.

One method is to increase government purchases in the hope that this will provide money to those with a high propensity to consume. This "pump-priming" will then supposedly revitalize a depressed economy back to health. Much like buying bonds to reduce interest rates, this process at first appears to work. The failure is not in Keynes observation. It occurs when government attempts to finance its purchases.

When the purchases are financed by taxation or borrowing these fiscal actions become a drag on the economy countering the pump-priming tendency to revitalize the economy. This problem has caused the geniuses of economic analysis to insist the pump- priming must come from expansion of the money supply. Expansion of the money supply transfers value from those who hold money to those who hold real assets and to the creator of the money -- the government. Which group may have more propensity to consume is only circumstantial. It is these circumstances, not expansion of the money supply, that determines the outcome of this process.

Keynes proposed to deal with the problem of the Great Depression by having the government hire people to bury cans of money and let the unemployed dig it up. This proposal may sound a bit ludicrous but, unlike the proposals of more recent Keynesians, this would at least have accomplished its purpose of getting money to those with a propensity to consume. A more rational approach to accomplish this goal of distributing the abundance of nature to those with need is available when the self righteous beliefs of those who insist we must earn our keep from those who have absconded with the substance of nature is dispatched. But, more on that later.

There is one thing in common to all of these arguments. That is that they all admit that the value of money depends on the quantity of money relative to the level of economic activity. They then assume that creation of money will cause economic activity to increase and that the increase in economic activity will be sufficient to keep the value of money from falling. But, one must ask -- By what mechanism does money creation cause economic activity?

Despite all the pretentious arguments to the contrary, any reasonable consideration of this question must conclude that the only economic activity caused is the readjustment of individual assets to reflect any suspected changes in the future value of money. This is not to say that the quantity of money is insignificant to economic activity. But in and of itself money does not produce wealth. And making its value less certain can hardly improve the efficiency of exchange promoted by its use.

The value of money is affected by many things, most of which are beyond measure and control. Such things as war, pestilence, fire, drought and inflationary expectations all affect the value of money. And there are many other things that may either contribute to the determination of its value or may themselves be affected by the value of money, its expected value or uncertainty in its expected value. But, the value of money is also affected by the quantity of money and money substitutes relative to the demand for money. Central bank open market operations directly affect the supply of demand deposits, a form of money in all economists' definitions of money. And, central bank open market operations can be both measured and controlled.

There are many ways to express the value of money. It can be expressed as the quantity of gold that a particular quantity of money will buy or as the reciprocal of this -- the price of gold. It can also be expressed as a price index of commodities such as the Producer Price Index. But the most meaningful of the measures of money value is the weighted average of prices contained in the Consumer Price Index. This is not to say the Consumer Price Index is the best way to measure the value of money. There may be better methods. But among the presently available choices it is the Consumer Price Index that is used for most wage and other contract price adjustments and it is the index that most people accept as the measure of inflation.

Some confusion does exist between the measure and the thing being measured -- Consumer Price Index and money value. The confusion is not the difference of one being the reciprocal of the other. That is a tautology. The confusion is the distinction between the frequency of measurement of the Consumer Price Index and the frequency of changes in the value of money. Monthly measurement of the index is a limit imposed by practical considerations but change in the value of money occurs in infinitesimally small increments billions of times a day.

For example: Let us say that the price of bread is one-tenth of one percent of the Consumer Price Index. Let us further say that for purposes of measuring the CPI the price of bread is defined as the average price of the most recent one-million loaves sold. Then each time a loaf of bread is sold the value of money in terms of the Consumer Price Index changes one-tenth of one percent of one-one millionth of the difference between the price of the most recent sale and the price of the loaf sold a million and one loaves ago. A similar infinitesimal change occurs every time any of the thousands of things included in the Consumer Price Index is sold. Just because it has not been calculated does not change the reality that the value of money changes, up or down, with each transaction.

This distinction between the measurement and the thing measured may at first seem trivial. But it is such trivialities that underlie the ease with which circumlocutious nonsense passes as analysis. Change in the value of money is not a spontaneous change occurring only with each measurement. It is the result of the cumulative effect of changes that occur with every exchange of every item that is included in the definition of the value of money.

While controlling the value of money might result in a nearly constant rate of increase in the quantity of money it does not hold that a constant rate of increase in the quantity of money -- one of the proposed schemes for monetary policy -- will result in a nearly constant value of money. The presumption that growth in the money supply is either sufficient or necessary to promote economic growth -- another scheme -- is nothing but wishful thinking.

It is the problem of the direction of cause and effect that makes control of the quantity of money a poor substitute for direct maintenance of the value of money and it is the lack of any causal relationship between money creation and economic growth that makes the use of monetary policy to promote economic activity a fabrication of incompetent analysis.

Statistical correlations make no distinction as to cause or effect but, because it is already recognized that central bank open market operations can control the quantity of money or credits and relative changes in the quantity does affect the value of money, it is not necessary to know the chain of cause and effect of other things used to determine the specific amount of control needed. All that is required is that the things used be subject to measurement. If it were possible to measure the effect on money value of war, pestilence, fire and drought these would be useful items to include in the correlation equations. But, alas, this is not to be.

Fortunately, there are many items that are both measurable and reflect the cumulative decisions to reallocate the demand deposits created or destroyed by the Federal Reserve System.These are things such as the various components of economists' definitions of money supply, categories of bank loans and investments and the recent behavior of inflation as reflected in the Consumer Price Index. The net result of Federal Reserve System open market operations, the only item affecting money value that can be directly controlled, is measured by the amount of government debt held by Federal Reserve Banks.

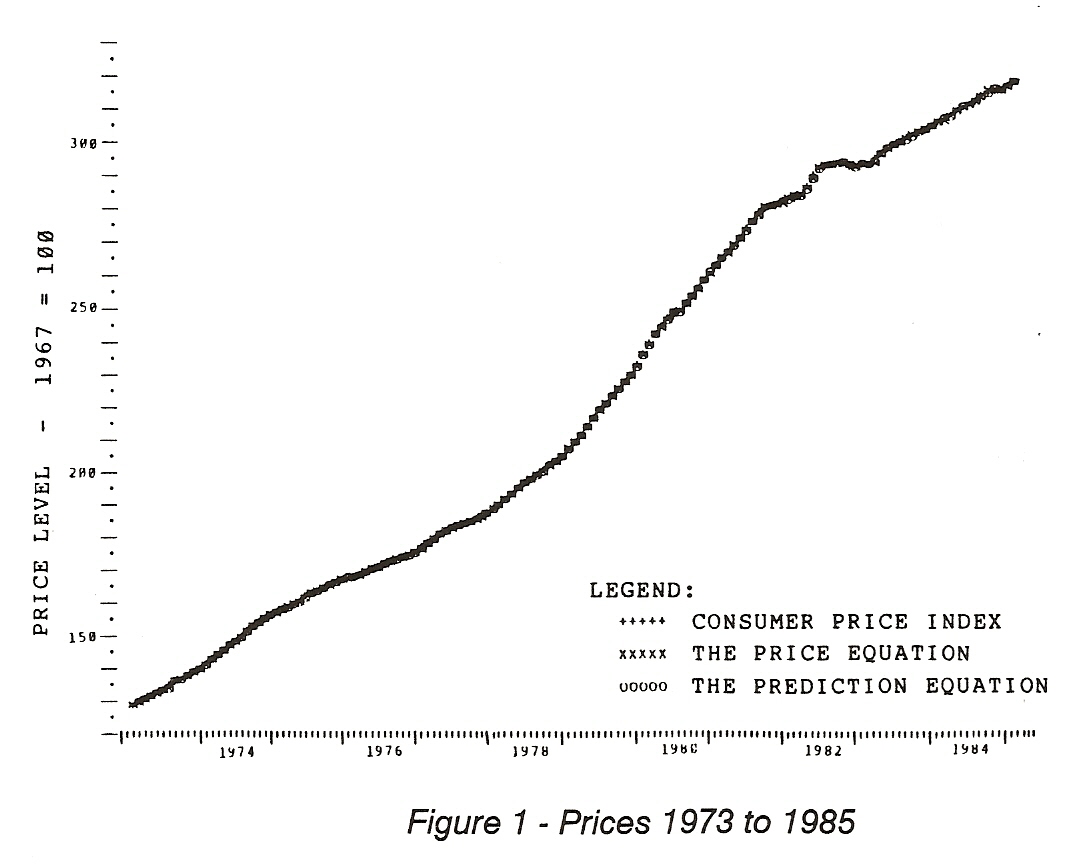

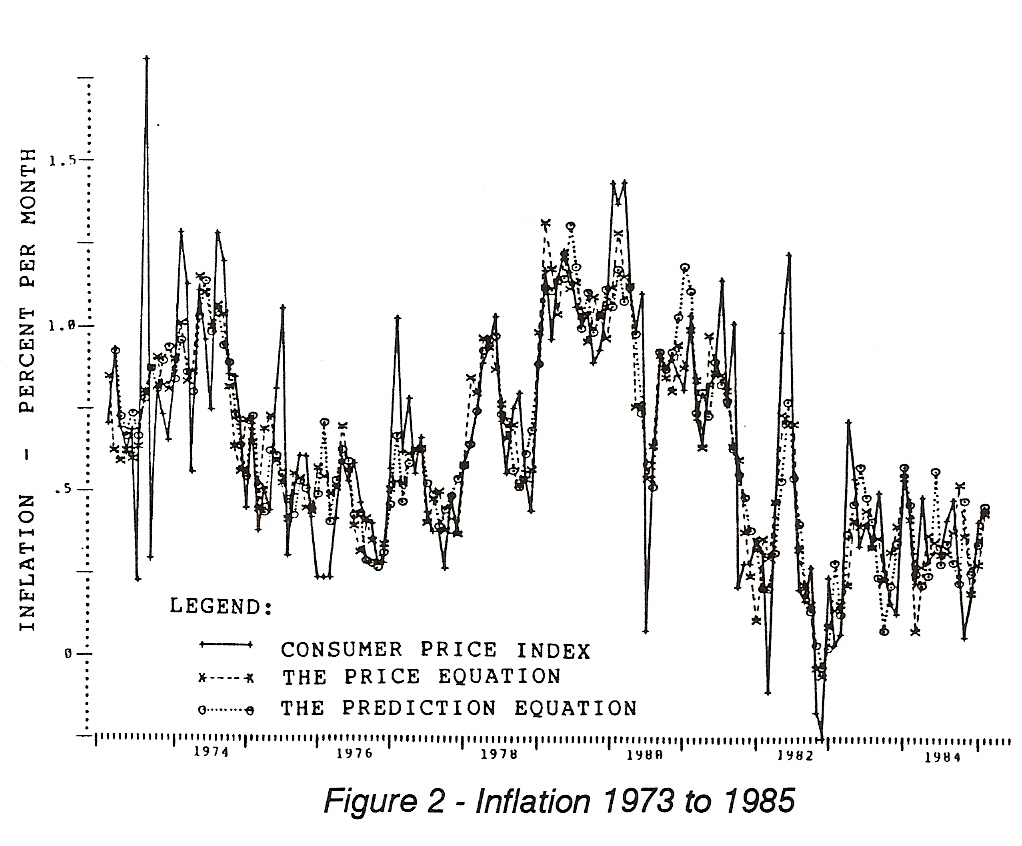

The technical details of the correlations with this data are shown in

Table 1 and Table

2. But, as they say, numbers are just numbers but a picture

is worth a thousand words. Figure 1 shows the measured value of

the Consumer Price Index, a computed value based on the price equation

shown in Table 1 and a predicted value from the prediction equation

shown in Table 2.

Control can be attained in only two ways: (1) by accurate prediction of the amount of control required or, (2) by a compensating response to undesired changes. To control the value of money it is necessary to know beforehand how much money is required to attain the particular value of money desired or else each change in money value must be corrected after the fact so that the changes do not accumulate over time.

Because the prediction equation shown in Table 2 uses only known values of the measures used in the computations plus the net result of Federal Reserve System open market operations during the prediction month, this equation can be solved for the required amount of control to maintain a constant value of the Consumer Price Index. That is, by taking the prediction equation, setting the inflation rate to zero, solving for the required amount of government debt to be purchased or sold by the Federal Reserve System then monetary policy can be directed to maintain a constant value of money.

This method, attempting to control money value by accurate prediction, misstates the true importance of these correlations. It assumes that existing circumstances, uncertain future value of money, that influence the correlation constants will not change under circumstances of a constant value of money. An obvious absurdity. The true import of these correlations is based on the evidence they provide in support of the second method of control -- responding to undesired changes. There are two results of significance. The first is:

Interest rates can be said to be composed of two parts:

Another effect of a constant value of money is a substantial improvement in the quality of business decisions. That is, without the problem of uncertainty in the future value of money business decisions can be made with only the normal risk of the market place. Businesses can pursue their activities without the devastating risk of cyclical variations in money value caused by government manipulation.

The effect a constant value of money will have on the current crisis of debtor nations and their credit suppliers can hardly be imagined. But, it certainly would be positive.

The second significant result of these correlations derives from elimination of inflation and monetary considerations from analysis of economic growth. With elimination of that false assumption analysis of economic growth shows:

Return to Contents Page

Return to Home Page