Entrepreneurship – Grade 12

Alternative Delivery Mode

Quarter 2 - Module 10

First Edition, 2020

Republic Act 8293, section 176 states that: “No copyright shall subsist in any work of the Government of the Philippines. However, prior approval of the government agency or office wherein the work is created shall be necessary for exploitation of such work for profit. Such agency or office may, among other things, impose as a condition, payment of royalty.”

Borrowed materials included

in this module are owned by the respective copyright holders. Effort has been

exerted to locate and seek permission to use these materials from the

respective copyright owners. The publisher and author do not represent nor

claim ownership over them. Published by

the Department of Education – Region X – Northern Mindanao Regional Director: Dr. Arturo B. Bayocot, CESO V

Borrowed materials included

in this module are owned by the respective copyright holders. Effort has been

exerted to locate and seek permission to use these materials from the

respective copyright owners. The publisher and author do not represent nor

claim ownership over them. Published by

the Department of Education – Region X – Northern Mindanao Regional Director: Dr. Arturo B. Bayocot, CESO V

Development Team of the Module:Development Team of the Module

Authors: Joel Y. Yacas Janice B. Dominguez

Author: Naneth M. Valdehuesa Joel Y. Yacas Ronee D. Quicho Janice B. Dominguez

Mary Cris A. Maquilan Naneth M. Valdehuesa Ronee D. Quicho Marylinda T. Puzon

Charity E. Parel Mary Cris A. Maquilan Marylinda T. Puzon Denver E. Neri

Lorena Fe S. Anub Charity E. Parel Denver E. Neri Ethel Lalaine B. Morales

Lorena Fe S. Anub Ethel Lalaine B. Morales

Evaluators: Evaluators: Cherryl F. Descallar Cherryl F. Descallar Eddy Lou T. Hamak

Sherriemae V. Reazol Eddy Lou T. Hamak

Sherriemae V. Reazol

Reviewers:

Illustrator: PSSg Edzel M. Dominguez

Illustrator: PSSg Edzel M. Dominguez

Layout Artist: Management Team:

Management Team: Chairperson: Dr. Arturo B. Bayocot, CESO III

Chairperson: Dr. Arturo B. Bayucot, CESO III Regional Director

Co-Chairpersons: Dr. Victor G. De Gracia Jr., CESO V

Regional Director

Asst. Regional Director

Co-Chairpersons: Dr. Victor G. De Gracia Jr., CESO V Mala Epra B. Magnaong

Asst. Regional Director CES, CLMD

Members: Dr. Bienvenido U. Tagolimot, Jr.

Mala Epra B. Magnaong

Regional ADM Coordinator

CES, CLMD Elson C. Jamero

Members: Dr. Bienvenido U. Tagolimot, Jr. EPS-Designate-TLE Rone Ray M. Portacion

EPS-ADM EPS-LRMS

Printed in the Philippines by: Department of Education – Bureau of Learning Resources (DepEd-BLR) Printed in the Philippines by: Department of Education – Regional Office 10

Office Address:Office Address: Zone 1, Upper Balulang Cagayan de Oro City 9000 Masterson Avenue, Upper Balulang, Zone 1, Cagayan de Oro City, Cagayan de Oro,

Telefax:

(088) 880-7071, (088) 880-7072Lalawigan ng Misamis Oriental E-mail Address:

TABLE OF

CONTENTS

TABLE OF

CONTENTS

|

What I Need to Know ………......................................... What I Know ………......................................... Lesson 1: Perform Bookkeeping Tasks What’s In ……………………………………. What’s New ……………………………………. Lesson 2: Prepare an Income Statement and a Balance Sheet Income Statement ……………………………………. Balance Sheet ……………………………………. Lesson 3: Identify where there is a Profit or Loss for a Business Net Income/Loss ……………………………………. Lesson 4: Interpret Financial Statement Interpretation of Financial Statements ………………………. What is It ……………………………………. What’s More ………......................................... What I Have Learned ………......................................... What Can I Do ………......................................... Assessment ………......................................... Additional Activities ………......................................... Quarter Challenge 2 ……………………………………. Answer Key ………......................................... References ………......................................... |

43 54 76 87 2019 2120 2423 2524 4140 4443 4544 4544 4746 4948 5150 5857 7170 |

What I Need to Know

Welcome to this module. In this module you will learn how to record business transactions, generate financial information and communicate them to different users. This is your tool to keep track of the operations of your business, know how much should you collect, determine your capability to meet the currently maturing obligations, know the levels of your profitability, cash position, and communicate them to management and other interested parties such as the Bureau of Internal Revenue and Local Government Unit for tax and regulation purposes.

This module is divided into four lessons:

Lesson 1 – Perform bookkeeping tasks

Lesson 2 – Prepare an income statement and a balance sheet,

Lesson 3 – Identify where there is a profit or loss for a business,

Lesson 4 – Interpret financial statements (balance sheet, income statement), cash flow projections, and summary of sales and cash receipts

To be able to completely learn this module, you need to know and understand the basic concepts of bookkeeping and apply the same by performing bookkeeping tasks, prepare income statement and balance sheet, interpret financial statements, identify whether the business is profitable or not and most importantly, you will be able to generate overall report on the company’s financial status.

Before starting with this module, let us evaluate what you already know about bookkeeping by answering the pre-assessment questions below.

TEST I – Multiple Choice: Identify the correct answer among the given choices. In your answer sheet, write the letter only.

1. A source document evidencing that orders have been placed by the customer waiting to be served by the supplier

A. Purchase request B. Purchase order

C. Purchase invoice D. Purchase check

2. The source document evidencing that goods have been delivered by the supplier to the customer-

A. Supplier’s sales invoice C. Customer’s sales invoice B. Vale slip D. Customer’s delivery receipt

3. A source document issued by the supplier acknowledging that full payment has been received from the customer-

A. Official receipt C. Delivery receipt

B. Purchase receipt D. Receiving report

4. Is a statement of the financial position of a business which states the assets, liabilities, and owners' equity at a particular point in time.

A. Balance Sheet B. Income Statement C. Owner’s Equity D. Assets

5. A source document which accompanies a check when payment is made-

A. Check voucher C. Cash voucher

B. Purchase voucher D. All of the above

6. All of the following are examples of source documents, except-

A. Check B. Invoices C. Contract D. Journal

7. A source document which shows that the customer has already made partial payment to the supplier through issuance of-

A. Check B. Voucher C. Official receipt D. Sales Invoice

8. Are things or properties that the business owns, example includes cash, account receivable and prepaid expenses.

A. Assets B. Liabilities C. Owner’s Equity D. Revenue

9. It is the obligations of the company, payable in money, goods or services.

A. Assets B. Liabilities C. Owner’s Equity D. Revenue

10. It is the claim of the owner of the business also known as the capital.

A. Assets B. Liabilities C. Owner’s Equity D. Revenue

11. ________ is a record comprising the sales and other income recieved by the

business.

A. Assets B.

Liabilities C. Owner’s Equity D. Revenue

12. The most liquid form of asset

that can be used anytime to purchase another

assets or pay liabilities.

A. Inventories B. Receivables C. Payable D. Cash

13. An example of asset that can be used in the business for a long period of time.

Usually more than a year.

A. Inventories B. Computer C. Receivables D. Cash

14. A type of business that is purely engage in providing all types of service activities such as medical or legal services.

A. Service Business C. Manufacturing business

B. Merchandising business D. Trading Business

15. A type of business that is engage in buying and selling of food products such as Grocery/convenient stores.

A. Service Business C. Manufacturing business

B. Merchandising business D. Forex Trading Business

|

Lesson 1 |

Perform Bookkeeping Tasks |

In the previous lesson, you learned how to make and prepare a business plan, operate the business, know how to sell the product, and the significance for keeping business records.

A business plan is an effective tool in making your dream business come true.

It reiterates different plans or strategies in Operation and Administration, Marketing, Production and Logistics, Finance, etc.

The operational plan put into details on what business model you are going to employ and how are you going to start the business. Among others, its also reiterated the layers pf management, type of skills and employee attitude your business need and the steps on how to get the government license.

The marketing plan contains valuable strategies as to what product your are going to produce or sell, what industry you want to enter, group of target customers, or your target market and the business model or strategies you are going to employ.

The production plan revealed the production processes and the quality control system of the goods produced for sale. While the logistics provides a channel of distribution of the goods from production lines down to the wholesellers/retailers or directly to consumers.

The financial plan talks about monetary requirements before you open the business. While financial forcast informs the business owners of the expected outcome of the business in monetary terms.

What is Bookkeeping?

Bookkeeping is the process of recording business transactions in a systematic and chronological manner.

It is systematic because it follows procedures and principles. On the other hand, it is chronological because the transactions are recorded in order of the date of occurrence.

Bookkeeping is the starting point of the accounting process. A sound bookkeeping system is the foundation for gathering the information necessary to answer questions related to profitability, solvency and liquidity of the business.

What is a Bookkeeper?

Each business has a bookkeeper who is incharge to record, maintain and update business records from all sorts of financial transactions using account title that can be found in the charts of accounts already set up by the Accountant.

The bookkeeping function dictates the bookkeeper to keep track of all financial transactions of the business. Only transactions that has monetary value will be recorded.

The bookkeeper uses the Book of Accounts to record the business

transactions which is to be consolidated later to help construct financial statement such as the Trial Balance, Income Statement and Balance Sheet.

What is a Book of Account?

The book of accounts are composed of the Journal and Ledger. It depends on the type of business, some businesses used special journals when they are engaged merchandising type of business to records business transactions. This module will cover and provide example for service oriented business. Thus, only journal and ledger will be used in the succeeding examples.

There are two types of books used in recording business transactions. They are called journals and ledgers.

Journal refers to the book of original entry while the Ledger refers to the book of final entry.

What is a General Journal?

The general journal is the most basic journal which provides columns for date, account titles and explanations, folio or references and a separate column for debit and credit entries. Depicted in figure 1 below is a sample format of a general journal:

What is a General Ledger?

The general ledger is a grouping of all accounts directly traceable to chart of accounts. These accounts will be reflected in the financial statements as a summary of all financial activities that have taken place as recorded in the general journal and subsidiary ledgers. Depicted in figure 2 below is a sample format of a general ledger:

What is a Subsidiary Ledger?

The subsidiary ledger is a group of accounts directly associated from the general ledger. This record is created to maintain individual accounts for customers and vendors whose cash is not being used as a medium of exchange when purchasing or selling merchandise. Depicted in figure 3 and 4 below is a sample format of a subsidiary ledgers Accounts Receivable and Accounts Payable respectively:

The Rules of Debit and Credit

In the process of journalization, following the rules of Debit and Credit are essential part to ensure accurate recording and sound decision making. Debit is abbreviated as DR while CR for Credit.

It is a requirement that the bookkeeper is able to master the normal balance of each account title before performing the tasks of bookkeeper.

When to Debit?

When cash or non-cash items are received, the said cash or non-cash items must be recorded in the debit column. This means that the debit balance increased. It is called Value Received.

When to Credit?

When cash or non-cash items are given, the said cash or non-cash items must be recorded in the credit column. This means that the credit balance is increased. It is called Value Parted With.

The following steps will be undertaken in determining account balances for every account title such as cash, account receivable, etc.:

1. Add all the debit side to generate total debit 2. Add all the credit side to generate total credit.

3. Subtract total debit to the total credit.

4. Determine the balance of each account.

Depicted in figure 5 below is a matrix of normal debit and credit balances of Five Major Accounts:

|

Account Type |

Debit |

Credit |

|

Assets |

|

|

|

Liabilities |

|

|

|

Owner’s Equity |

|

|

|

Revenue |

|

|

|

Expenses |

|

|

Figure 5 - Matrix of Normal Debit and Credit Balances

of Five Major Accounts

In order to fully understand the concept of debit and credit balances, depicted in figure 6 below is a matrix of normal debit and credit balances under each of the five major accounts:

|

Account Type |

Debit |

Credit |

|

|

Assets |

|

|

|

|

|

Cash on Hand |

|

|

|

|

Cash in Bank |

|

|

|

|

Accounts Receivable |

|

|

|

|

Allowance for Doubtful Accounts |

|

|

|

|

Notes Receivable |

|

|

|

|

Prepayments |

|

|

|

|

Inventories |

|

|

|

|

Land |

|

|

|

|

Building |

|

|

|

|

Equipment |

|

|

|

|

Accumulated Depreciations |

|

|

|

|

Other Assets |

|

|

|

Liabilities |

|

|

|

|

|

Accounts Payable |

|

|

|

|

Notes Payable |

|

|

|

|

Salaries Payable |

|

|

|

|

Mortgage Payable |

|

|

|

|

Unearned Fees |

|

|

|

Owner’s Equity |

|

|

|

|

|

Capital |

|

|

|

|

Drawing |

|

|

|

Revenue |

|

|

|

|

|

Service Income |

|

|

|

|

Other Income |

|

|

|

Expenses |

|

|

|

|

|

Rent Expense |

|

|

|

|

Utilities Expense |

|

|

|

|

Depreciation Expense |

|

|

|

|

Salaries and Wages Expense |

|

|

|

|

Other Expenses |

|

|

Figure 6 - Matrix of Normal Debit and Credit Balances

of Sub-accounts

TRIAL BALANCE

Trial balance is a list of all ledger accounts with closed or final balances on a certain period arranged according to the rules of debit and credit. The debit and credit columns must be equal in total amount. This is the first report prior to financial statement preparation. Depicted in figure 7 below is a sample format of a trial balance report with peso amount.

As you can observed, the accounts reflected in figure 7 above are arranged according to the proper placement of the five major accounts. The Assets, Liabilities, Owner’s Equity, Revenue and Expense accounts. You may refer to figure 6.

On the other hand, the trial balance report has two phases. The first phase “Unadjusted trial balance” is a report of all balances after the posting of the general ledger accounts. The general ledger account balances are extracted to construct the unadjusted trial balance. Meanwhile, the second phase is the “Adjusted trial balance”. This phase is a final report of trial balance after all necessary adjustments in journal entries are posted in the general ledger.

What is an Adjusting Entry?

Making an adjusting entry helps the bookkeeper capture all financial events happened over a period of time within the accounting cycle. It is essential in keeping the financial record updated. The bookkeeper is going to look or examine accounts that needs to be updated. Outlined below are the five basic sources of adjusting entries:

1. Depreciation expense

2. Deferred expenses of prepaid expenses

3. Deferred income of unearned income

4. Accrued expenses of accrued liabilities

5. Accrued income or accrued assets

This is a method of allocating the cost of an asset to an expense over the accounting periods that make up the asset’s useful life. Examples of assets subject to depreciation are: Store, Office, Building, and Transportation equipment. These types of assets lose their ability to provide useful service as time passes. Depreciation can also be referred to as the decrease in the usefulness of these types of assets. Take note that Land is not subject to depreciation because the value of land mostly increases as time passes.

There are several methods or formulas to compute the amount of depreciation.

The simplest is the straight-line method.

The formula:

Where:

• Acquisition cost – the actual cost of the asset acquired.

• Salvage value – the selling price of the asset upon reaching the useful life.

• Useful life – is the economic or productive life of the asset.

Illustrative problem:

The cost of the equipment is PHP25,000. It was estimated to have a useful life of five years. It is estimated that after five years, the office equipment can be sold at a scrap value of PHP1,000. To compute for the monthly depreciation, just divide the annual depreciation by 12. One year is composed of 12 months.

- (5 yrs x 12 mos. = 60 months)

Adjusting entry:

GENERAL JOURNAL PAGE 1

![]()

|

|

|

|

POST. |

|

|

|

|

DATE |

P A R T I C U L A R S |

REF. |

DEBIT |

CREDIT |

||

|

1 |

June |

30 |

Depreciation expense |

|

400.00 |

|

|

2 |

|

|

Accumulated depreciation – (equipment name) |

|

|

400.00 |

|

3 |

|

|

To record the allocation of depreciation expense |

|

|

|

The depreciation expense is an allocated for all sixed assets except land. Example are building, equipment and or machineries that the business is using to generate income. It shall be reported as an expense account in the income statement directly attributable in the said fixed assets. While the accumulated depreciation is a balance sheet account but treated as a contra-account to the concerned fixed asset.

Refer to the illustration below:

Balance Sheet

As of ____________

…

Equipment (at cost) P 25,000

Less: Accumulated Depreciation-Equipment 400

Net Book value of Equipment P 24,600

These are items that have been initially recorded as assets but are expected to become expenses over time or through the operations of the business.

In order to recognize the correct amount of expenses, prepayments shall be amortized weekly, semi-monthly or monthly, depending on its nature and purpose.

Illustrative problem:

Purchased P5,000 worth of office supplies on account. By the end of the month, PHP2,000 worth of these supplies are still unused.

Adjusting entry:

GENERAL JOURNAL PAGE 1

![]()

|

|

|

|

POST. |

|

|

|

|

DATE |

P A R T I C U L A R S |

REF. |

DEBIT |

CREDIT |

||

|

1 |

June |

30 |

Supplies expense |

|

3,000 |

|

|

2 |

|

|

Supplies |

|

|

3,000 |

|

3 |

|

|

To set up the value of used supplies. |

|

|

|

The supplies expense is an income statement account, while the supplies which is now credited is an asset account. All asset has a normal debit balance. Considering that the supplies in this record is credited. This will be deducted to the supplies account in the balance sheet to generate the remaining balance in supplies.

These are items that have been initially recorded as liabilities but are expected to become income over time or through the operations of the business.

Illustrative problem:

On February 15, 2016 Matapang entered into a contract with Makisig to maintain the computers of Makisig for two months starting on February 15, 2016 up to April 15, 2016. On the same date, Makisig paid the total contract amount of PHP40,000 in full. The entries to record and adjust the books are: In the February 29, 2016 entry above, as of end of February 2016, Matapang has already earned the service revenue for the first 15 days, thus an adjusting entry is recorded.

![]()

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

Journal entry: |

|

|

|

|||

|

1 |

Feb |

15 |

Cash |

|

40,000 |

|

|

2 |

|

|

Unearned service revenue |

|

|

40,000 |

|

3 |

|

|

To record receipt of full payment for the two-month service contract with Makisig |

|

|

|

|

Adjusting entry: |

|

|

|

|||

|

4 |

Feb |

29 |

Unearned Service Revenue |

|

10,000 |

|

|

5 |

|

|

Service Revenue |

|

|

10,000 |

|

6 |

|

|

To record service income earned from Feb 15-29, 2016; P40,000 x (1/2 month /2 months) |

|

|

|

These are items of expenses that have been incurred but have not been recorded and paid.

Illustrative problem:

On February 29, 2016, Matapang received the electric bill for the month of February amounting to PHP3,800. Matapang will pay this bill on March 2016. The electric bill represents the cost of electricity used (or incurred) for February. Although the said bill is still unpaid and thus was not recorded, the matching principle and accrual basis of accounting dictates that the same should be recorded in February. Otherwise, your expense will be understated and thus the company will be reporting an overstated income (or an erroneous income). Needless to say, erroneous information may lead to wrong decisions. The entry to record the accrual of this expense is:

Adjusting entry:

![]()

|

|

|

|

POST. |

|

|

|

|

|

DATE |

P A R T I C U L A R S |

REF. |

DEBIT |

CREDIT |

|

|

1 |

Feb |

29 |

Utilities Expense |

|

3,800 |

|

|

2 |

|

|

Utilities Payable |

|

|

3,800 |

|

3 |

|

|

To accrue the cost of electricity incurred for the month of February. |

|

|

|

These are income items that have been earned but have not been recorded and paid by the customer. In short, these are receivables of the business.

Illustrative problem:

On February 28, 2016, Matapang repaired the computer of Pedro for

PHP15,000. Pedro was on an out-of-town trip so he could not pay Matapang. He told Matapang that he will pay for their services on March 1, 2016. Matapang has already earned the PHP15,000 but was not paid as of the end of February 2016. Therefore, an income should be properly recognized in February 2016 for this transaction. The entry to record this is: Adjusting entry:

![]()

|

|

|

|

POST. |

|

|

|

|

|

DATE |

P A R T I C U L A R S |

REF. |

DEBIT |

CREDIT |

|

|

1 |

Feb |

29 |

Accounts Receivable |

|

15,000 |

|

|

2 |

|

|

Service Income |

|

|

15,000 |

|

3 |

|

|

To record accrued income for the services already rendered during the month of February. |

|

|

|

|

Lesson 2 |

Prepare an Income Statement and a Balance Sheet |

This statement is one of the major financial report. Also known as profit and loss statement or statement of comprehensive income. This statement summarizes the results of company’s operations for a specific period of time. If the result of operation is positive, then the business earns net income otherwise, net loss.

Ledger accounts that can be found in the income statement are called Temporary accounts of Nominal accounts. They are called such because at the end of the accounting period, balances under these accounts are transferred to the capital account, thus having only temporary amounts and resulting to zero beginning balances at the beginning of the following year.(Haddock, Price, & Farina, 2012) Examples of temporary accounts include revenues, sales, utilities expense, supplies expense, salaries expense, depreciation expense, interest expense among others.

Depicted in figure 8 below is sample format of an income statement.

The different parts of income statement are:

• The heading or title of report

• Name of the company

• Date or period covered Major parts are:

• Income or revenues - consist of all income received within the period upon provision of services for service-concern business and sales for merchandising

• Expenses – money spent during the conduct of business operations Net income / net loss – the outcome of business operations.

BALANCE SHEET

Also known as the statement of financial position. This statement summarizes the total balances of assets, liabilities and owner’s equity. In general, it provides the financial condition of the business on a specific date.

The balance sheet is composed of Permanent accounts. Permanent in nature

because their balances remain intact and will be forwarded from one period to another.

Contra asset are those asset account presented under the asset portion of the balance sheet such as Allowance for Bad debts and Accumulated depreciation. Depicted in figure 9 below is sample format of a balance sheet of a service type business presented in as an account format with contra asset account.

The different parts of balance sheet are:

• The heading or title of report

• Name of the company

• Date or period covered

Major parts are:

• Assets (Current and Non-current)

Current Assets – Assets that can be realized (collected, sold, used up) one year after year-end date. Examples include Cash, Accounts Receivable,

Merchandise Inventory, Prepaid Expense, etc.

Current Assets are arranged based on which asset can be realized first (liquidity). Current assets and current liabilities are also called short term assets and shot term liabilities.

Noncurrent Assets – Assets that cannot be realized (collected, sold, used up) one year after yearend date. Examples include Property, Plant and Equipment (equipment, furniture, building, land), Long Term investments, Intangible Assets etc.

• Liabilities (Current and Non-current)

Current Liabilities – Liabilities that fall due (paid, recognized as revenue) within one year after year end date. Examples include Notes Payable, Accounts Payable, Accrued Expenses (example: Utilities Payable), Unearned Income, etc.

Noncurrent Liabilities – Liabilities that do not fall due (paid, recognized as revenue) within one year after year-end date. Examples include Loans Payable,

Mortgage Payable, etc.

Noncurrent assets and noncurrent liabilities are also called long term assets and long-term liabilities.

Capital is an item of balance sheet wherein the capital or interest of the owner of the business is listed. Initial withdrawal of capital will be recorded in a drawing account of the owner and will be reflected as a deduction to the capital balance.

|

Lesson 3 |

Identify where there is a Profit or Loss for a Business |

Profitability has always been the overall goal of the business. It is of great achievement in a successful implementation of strategic, operating and other plans.

In identifying the profit or loss of a business, the business will record every detail of all business transactions and translate it into financial report. An income statement is a financial report that reveals the total revenue or income, total expenses incurred during the conduct of the business and, most of all the net profit or net loss as a result of business operations over a specified period of time.

Below is the basic equation of income statement of a service-concern business:

|

Lesson 4 |

Interpret Financial Statements (Balance Sheet, Income Statement, Cash Flow Projections and Summary of Sales and Cash Receipts) |

Financial statements will reveal the outcome of the business operations. A financial analyst is like a medical doctor who will conduct diagnosis by reading the financial report and render interpretations on it which will be used as the basis of a sound economic decision making.

As previously defined, balance sheet reflects the financial position and condition of the business. The financial position refers to the assets of the business which will be financed by the liability and owner’s equity. On the other hand, financial condition refers to the situation wherein assets, liability and owner’s equity are used to maximize income. Also, assets, liability and owner’s equity may encounter growth or decline in value.

There are many available financing tools to be used in analyzing and interpreting financial statements. It depends on the purpose. Most of these tools are able to evaluate and interpret asset growth of the business, profitability, liquidity and solvency. In general, it will provide a bird’s eye view of the overall health of the business.

Depicted in figure 14 below is a matrix of financial interpretation with formula and explanation.

|

Accounts |

Formula |

Interpretation |

|

|

Profitability ratios |

Measure the ability of the company to generate income from the use of its assets and invested capital as well as control its cost |

||

|

|

Operating income ratio |

Operating Income Net Sales |

It measures the percentage of profit earned from each peso of (Horngren et.al. 2013). |

|

|

Return on asset (ROA) |

Net Income Ave. Assets |

Measures the peso value of income generated by employing the company’s assets. |

|

|

Return on equity (ROE) |

Net Income Ave. Equity |

Measures the return (net income) generated by the owner’s capital invested in the business |

|

Financial Health Ratios |

Refers to the company’s capacity to pay their short- and long-term obligations as they become due. |

||

|

Debt ratio |

Total Debt Total Assets |

Indicates the percentage of the company’s assets that are financed by debt. A high debt to asset ratio implies a high level of debt. |

|

|

Equity ratio |

Total Equity Total Assets |

Indicates the percentage of the company’s assets that are financed by capital. A high equity to asset ratio implies a high level of capital. |

|

|

Debt to equity ratio |

Total Debt Equity |

Indicates the company’s reliance to debt or liability as a source of financing relative to equity. A high ratio suggests a high level of debt that may result in high interest expense. |

|

|

Liquidity |

Measure the company’s ability to pay debts that are coming due (short term debt). |

||

|

Solvency |

Refers to the company’s capacity to pay their long-term liabilities. |

||

|

|

Current ratio |

Current Assets Current Liabilities |

It seeks to measure whether there are sufficient current assets to pay for current liabilities. Creditors normally prefer a current ratio of 2. |

|

|

Quick ratio |

Quick Assets Current Liabilities |

It does not consider all the current assets, only those that are easier to liquidate such as cash and accounts receivable that are referred to as quick assets. |

Figure 14 - Matrix of financial interpretation with formula and explanation.

ACTIVITY TIME: Now, let us complete the accounting cycle by recording financial transactions and applying the concept of bookkeeping which will generate financial statements. Upon completing this activity, you will be able to know the financial position, profitability and the condition of the business thru financial statement analysis and interpretation.

Activity 1 : Identifying and

recording a business transaction using the General Journal

Activity 1 : Identifying and

recording a business transaction using the General Journal

Below is an example of business transactions of a service type business. You are task to record the said transactions in the general journal by means of journal entry applying the rules of debit and credit.

Depicted in figure 11 is the standard chart of accounts of Alpha Laundry

System.

Let us begin!

Mr. Denver Ambrose is a retired public school teacher. He started his laundry business in June 2018. He used all of his savings to start a “coin-operated laundry” business. He named it Alpha Laundry Systems (ALS). The following are business transactions for the month of June 2018, the first month of business operation:

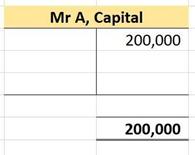

1. June 1, 2018 - Mr. A invested P 200,000 cash in his newly opened Alpha Laundry System business.

Your Journal Entry:

![]()

|

|

|

|

POST. |

|

|

|

|

DATE |

P A R T I C U L A R S |

REF. |

DEBIT |

CREDIT |

||

|

1 |

June |

1 |

|

|

|

|

|

2 |

|

|

|

|

|

|

|

3 |

|

|

To record the initial Capital investment of Mr. A. |

|

|

|

2. June 2, 2018 - Mr. A hired his former classmate Doree Dy to be the laundry operator of ALS for a fixed monthly salary of P10,000. The operator will be paid every quencina.

3. On June 5, 2018 – Alpha Laundry Systems purchased laundry equipment for cash, P150,000.

Your Journal Entry:

![]()

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

4 |

June |

5 |

|

|

|

|

|

5 |

|

|

|

|

|

|

|

6 |

|

|

To record the acquisition of Laundry equipment |

|

|

|

4. On June 6, 2018 – Alpha Laundry Systems paid cash in advance for the 1 year insurance coverage of laundry equipment for the whole year amounting to P6,000.

Monthly insurance expense will be recognized for each month end report.

Your Journal Entry:

![]()

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

7 |

June |

6 |

|

|

|

|

|

8 |

|

|

|

|

|

|

|

9 |

|

|

To record the prepaid Insurance for the Laundry equipment |

|

|

|

5. On June 7, 2018 – Alpha Laundry Systems bought supplies for laundry amounting to P10,000. The supplies bought are laundry consumables such detergent powder, soap bar and fabric softener. Monthly inventory will be conducted to determine unused supplies and will be recognized for each month end report.

Your Journal Entry:

![]()

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

10 |

June |

7 |

|

|

|

|

|

11 |

|

|

|

|

|

|

|

12 |

|

|

To record the acquisition of laundry consumables |

|

|

|

6. On June 15, 2018 – Alpha Laundry Systems paid P4,750 cash for salary of laundry operator.

Your Journal Entry:

GENERAL JOURNAL PAGE 1

![]()

|

|

|

|

POST. |

|

|

|

|

DATE |

P A R T I C U L A R S |

REF. |

DEBIT |

CREDIT |

||

|

13 |

June |

15 |

|

|

|

|

|

14 |

|

|

|

|

|

|

|

15 |

|

|

To record the payment of Laundry operator’s salary |

|

|

|

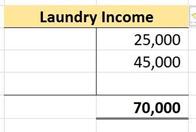

7. On June 16, 2018 – Alpha Laundry Systems received P25,000 cash for laundry services rendered to MZ. Hotel.

Your Journal Entry:

![]()

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

16 |

June |

16 |

|

|

|

|

|

17 |

|

|

|

|

|

|

|

18 |

|

|

To record the payment received from MZ Hotel. |

|

|

|

8. On June 17, 2018 – Alpha Laundry Systems rendered service to Argon Hotel amounting to P45,000. Argon promised to pay on June 20 of the same year.

Your Journal Entry:

![]()

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

19 |

June |

17 |

|

|

|

|

|

20 |

|

|

|

|

|

|

|

21 |

|

|

To record the service rendered to Argon Hotel |

|

|

|

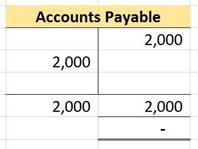

9. On June 18, 2018, Alpha Laundry Systems purchase office supplies from Ku Enterprises amounting to P2,000 on account. ALS will pay it on June 25 of the same year.

Your Journal Entry:

GENERAL JOURNAL PAGE 1

![]()

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

22 |

June |

18 |

|

|

|

|

|

23 |

|

|

|

|

|

|

|

24 |

|

|

To record the acquisition of Office Supplies on account from Ku Enterprises |

|

|

|

10. On June 20, 2018, Alpha Laundry Systems collected payment of Argon Hotel.

Your Journal Entry:

![]()

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

25 |

June |

20 |

|

|

|

|

|

26 |

|

|

|

|

|

|

|

27 |

|

|

To record the full payment from Argon Hotel |

|

|

|

11. On June 25, 2018, Alpha Laundry Systems paid in full the amount owed to Ku Enterprises.

Your Journal Entry:

![]()

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

28 |

June |

25 |

|

|

|

|

|

29 |

|

|

|

|

|

|

|

30 |

|

|

To record the full payment of account to Ku Enterprises |

|

|

|

12. On June 27, 2018, Alpha Laundry Systems paid electric bill for the month amounting to P1,000 in cash. The payment is charged to Utility expense account.

Your Journal Entry:

![]()

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

31 |

June |

27 |

|

|

|

|

|

32 |

|

|

|

|

|

|

|

33 |

|

|

To record the payment Electricity for the month |

|

|

|

13. On June 30, 2018, Alpha Laundry Systems paid a month’s transportation expense amounting to P 1,300.

Your Journal Entry:

![]()

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

34 |

June |

30 |

|

|

|

|

|

35 |

|

|

|

|

|

|

|

36 |

|

|

To record the payment of transportation for the month. |

|

|

|

14. On June 30, 2018, Alpha Laundry Systems paid P5,000 cash for salary of laundry operator.

Your Journal Entry:

![]()

|

|

|

|

POST. |

|

|

|

|

|

DATE |

P A R T I C U L A R S |

REF. |

DEBIT |

CREDIT |

|

|

37 |

June |

30 |

|

|

|

|

|

38 |

|

|

|

|

|

|

|

39 |

|

|

To record the payment Laundry operator’s salary. |

|

|

|

15. On June 30, 2018, Alpha Laundry Systems paid P7,500 cash for the month’s rent of laundry space.

Your Journal Entry:

![]()

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

40 |

June |

30 |

|

|

|

|

|

41 |

|

|

|

|

|

|

|

42 |

|

|

To record the payment of rent for Laundry space. |

|

|

|

Completing the monthly General Journal record will give the owner of the business a financial record of all business transactions that transpired during the month. It will reflect the inflows and outflows of cash, provisions of services which generate income.

The debit and credit columns should always be equal. Otherwise, the record will affect overall accuracy of the entire financial record. The error should be properly corrected before the next step in the recording process takes place.

![]() Activity

2 : Posting

journal entries to the General Ledger using T - accounts.

Activity

2 : Posting

journal entries to the General Ledger using T - accounts.

In this activity, you are task to post journal entries in the general ledger. The most convenient and fastest way of posting journal entries to the ledger is by way of using “T” Account. A T- Account is divided into two sides. The left- hand side is called the debit side and the right-hand side which is the credit side. The left -hand or debit side shows the value received while the right-hand side shows the value parted with.

This is called T account because it resembles capital letter “T.” an account title is written above the T- account.

After performing the T-accounts, balances for each account under Assets, Liabilities, Capital, Revenue/Income and Expenses, can now be determined.

Depicted in figure 12 below is a T-account and its description:

To strengthen your focus on the posting of journal entries to the general ledger, it is suggested to create T – account and label them with account title and group them according to Assets, Liabilities, Owner’s Equity, Revenue and Expense. Given below are T – accounts for all ledger accounts group according to the five major accounts.

|

ASSETS

|

LIABILITIES

OWNER’S EQUITY

|

|

REVENUE

|

EXPENSES

|

In this activity, you are task to create/prepare a trial balance for ALS. The period covered is June 2018.

You are going to pick up ledger account balances starting from cash, accounts receivable up to the last account in expense. Then, plot them in the trial balance report (un-adjusted trial balance). Compute for the total debit and credit balances. The debit amount should be equal to the credit.

![]() Activity 4 :

Record

adjusting journal entries in the General Journal.

Activity 4 :

Record

adjusting journal entries in the General Journal.

In this activity, you are task to identify accounts that needs to be adjusted.

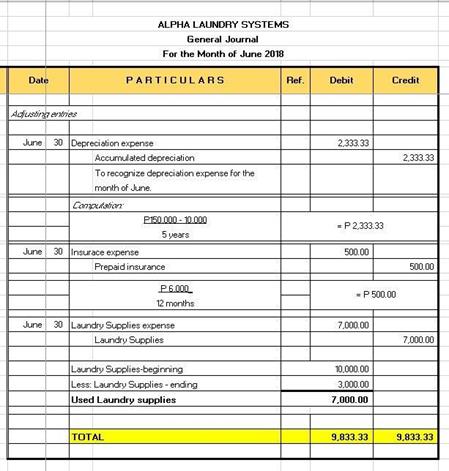

1. Depreciation of Equipment. The laundry equipment, which was purchased by

ALS on June 5, 2018 at P150,000 has an estimated useful life of 5 years with a salvage value of P10,000. Compute for the monthly depreciation to be charge as depreciation expense and will be deducted against the cost to get the net book value of the laundry equipment.

a. Compute for the monthly depreciation using straight line method.

Your Adjusting Entry:

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

43 |

June |

30 |

|

|

|

|

|

44 |

|

|

|

|

|

|

|

45 |

|

|

To recognize the depreciation expense for the month of June. |

|

|

|

2. Prepayments. The insurance paid for Laundry equipment is P6,000. An expired portion of the insurance in the amount of P 500 is determined by dividing the prepayments over 12 months (P6,000 / 12 months). The expired portion will be charged to expense. This will reduce the value of prepaid insurance balance.

a. Compute for the expired portion of the insurance.

To compute for the expired portion of the insurance:

Formula: Insurance Cost

Term of coverage = Expired insurance per month

(No. of Months)

Prepaid insurance P 6,000

Less: Expired portion (June) 500

Un-expired portion P 5,500

Note: The expired portion is charge to expense (insurance expense). The unexpired portion will be reported as the new prepaid insurance account balance for the next month.

Your Adjusting Entry:

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

46 |

June |

30 |

|

|

|

|

|

47 |

|

|

|

|

|

|

|

48 |

|

|

To recognize the expired portion of the prepaid insurance. |

|

|

|

3. Deferred expenses for supplies inventory. At the end of the month, unused supplies were recorded to be P3,000.

Note: The used supplies is charge to expense (supplies expense). The unused portion will be reported as the new supplies inventory balance for the next month.

Your Adjusting Entry:

GENERAL JOURNAL PAGE 1

|

|

|

P A R T I C U L A R S |

POST. |

|

|

|

|

DATE |

REF. |

DEBIT |

CREDIT |

|||

|

49 |

June |

30 |

|

|

|

|

|

50 |

|

|

|

|

|

|

|

51 |

|

|

To recognize the used portion of the Laundry supplies consumables |

|

|

|

Formula to compute for the used supplies:

Supplies at cost P 10,000

Less: Unused supplies 3,000 Used supplies P 7,000

![]() Activity 5 : Post adjusting journal entries in the General

Ledger.

Activity 5 : Post adjusting journal entries in the General

Ledger.

In this activity, you are task to post the adjusting entries written in the general journal to the general ledger and update the debit, credit and outstanding balances.

After doing so, you may proceed to the next activity.

![]()

In this activity, you are task to update the balance of all ledger accounts and transfer the balance to form a new adjusted trial balance. Still, the total debit and credit balances must be equal, if not you need to go back and review all entries and their corresponding amount to avoid errors and accuracy issues.

![]()

In this activity, you are task to segregate nominal accounts from permanent accounts. Only nominal accounts will be reflected in the income statement. Determine the debit and credit balances and deduct all expenses from revenue accounts in order to arrive at net income/loss.

How much is net income or loss of Alpha Laundry System?

The net income or loss can be determined upon finalization of income statements. Net income indicates that the business is profitable.

![]()

In this activity, you are task to segregate permanent accounts from nominal accounts. Only permanent accounts will be reflected in the balance sheet. Determine the debit and credit balances and compute for the total assets, total liabilities and total owner’s equity. The net income generated from the income statement must be added to the capital to generate total owner’s equity. If the business incur net loss, it will be deducted.

How much is the assets of the business? The assets of the business can be computed by adding up all assets accounts and deduct contra asset account. assets are used to generate income for the business.

As prescribed in the accouting equation, total assets must be equal to total liabilities and owner’s equity. Depicted in figure 13 below is the basic accounting equation.

![]()

What is cash receipt?

Cash Receipts include all of a firm’s inflows of cash in a given financial period. The most common components of cash receipts are cash sales, collections of accounts receivable, and other cash receipts.

What is a sales report?

A sales report is a record of all sales transactions. There are two type of sales transactions - cash sales and credit sales.

The amount received in cash sales transactions will be recorded in the cash receipt record book bearing the account cash. This will increase cash inflow. While the credit sales transactions cannot be recorded in the cash receipt record book because there were no inflows of cash. Instead, it will be recorded in the account receivable account. This means, that the business has a collectible account from a customer who bought the merchandise on his/her account.

What Is Cash Flow Projection?

A cash flow report records all cash inflow or out flow of the business.

Normally, it will report three business activities, namely, the operating, investing and financing activities.

The operating activities involves the main operations of the business which the buying supplies (cash outflow) and selling (cash inflow) of its products.

The investing activities involves the acquisition of long term or fixed assets of the business (cash outflow) and selling the old one’s cash inflow).

The financing activities involves the acquisition of capital of the business thru borrowings or investors (cash inflow) and payments of investors and creditors (cash outflow).

The cash flow projection is an important task of an accountant to determine the cash requirement for the next period of business operations. The business will be guided as to how much cash should be needed in order to pay operating expenses and how much cash should the business spend for fixed assets in order to increase sales, cash collection or a market share.

![]() Activity 9 : Interpret financial statements (balance sheet,

income statement, cash

Activity 9 : Interpret financial statements (balance sheet,

income statement, cash

flow projection and summary of sales and cash receipts.

|

Accounts |

|

Formula |

Answer |

|

|

Profitability ratios |

Measure the ability of the company to generate income from the use of its assets and invested capital as well as control its cost |

|||

|

|

Operating income ratio |

Operating Income Net Sales |

40,616.67 P70,000 |

58% |

|

|

Return on asset (ROA) |

Net Income Ave. Assets |

|

16.63% |

|

|

Return on equity (ROE) |

Net Income Ave. Equity |

|

20.31% |

|

Financial Health Ratios |

Refers to the company’s capacity to pay their short- and long-term obligations as they become due. |

|||

|

Debt ratio |

Total Debt Total Assets |

___0___ 242,950 |

0.% |

|

|

Equity ratio |

Total Equity Total Assets |

200,000 242,950 |

82.32% |

|

|

Debt to equity ratio |

Total Debt Equity |

___0___ 200,000 |

0.% |

|

|

Liquidity |

Measure the company’s ability to pay debts that are coming due (short term debt). |

|||

|

|

Current ratio |

Current Assets Current Liabilities |

|

|

|

|

Quick ratio |

Quick Assets Current Liabilities |

|

|

![]()

Discussion of activities:

Activity 1

In this activity, the bookkeeper was tasked to journalize all business transactions such as the buying and servicing or selling activities of the business. Transactions such as hiring new employees, signing contracts, surveying for new potential markets and making canvass for a merchandise to be purchased do not form part of the journalizing process. In making journal entries, i.e, using account title the bookkeeper should use the standard chart of issued by the company.

The bookkeeper will then compute for the total debit and credit column balances. The total general journal balance representing the debit and credit columns must be equal. Please refer to the General Journal.

Activity 2

In this activity, the bookkeeper was tasked to post journal entries in the general ledger. It is suggested that the posting process be done using T-account for faster and convenient way. Running balances of its account must be computed. The running balance must be placed according to the account’s normal balance following the rules of debit and credit.

The T-accounts of the activity was already available. The bookkeeper will only fill in the T-account of the specific account. Please refer to the T-account with running balances.

Activity 3

In this activity, the bookkeeper was tasked to transfer balances of each account in the T-account. The bookkeeper will then compute for the total debit and credit column balances. The bookkeeper must see to it that the debit and credit columns must be equal.

The un-adjusted trial balance can now be reported as partial financial report for the period prior to any end of month adjustments. Please refer to the Worksheet.

In this activity, the bookkeeper was tasked to identify accounts that needs to be adjusted. The bookkeeper will also use account titles available in the chart of accounts.

The adjustments are journalized in general journal on a separate page.

In this activity, the bookkeeper was tasked to post all adjustments in the general ledger or thru the use of T-account. such adjustments and will be reflected in the adjustment columns in the worksheet. The bookkeeper will then compute for the total debit and credit column balances. Please refer to the Worksheet.

In this activity, the bookkeeper was tasked to prepare Adjusted trial balance by updating all account balances horizontally, adding or subtracting accounts affected by the adjustments made.

The bookkeeper will then compute for the total debit and credit column balances. The bookkeeper must see to it that the debit and credit columns must be equal.

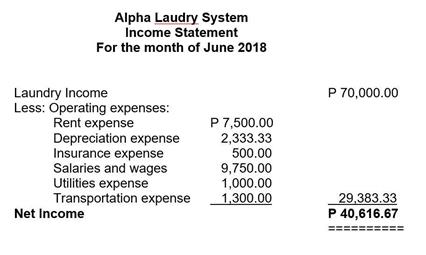

In this activity, the bookkeeper was tasked to prepare an Income Statement.

Nominal accounts are extracted from the adjusted trial balance to form income statement.

Below is the income statement of Alpha Laundry Systems:

In this activity, the bookkeeper was tasked to prepare Balance Sheet. Permanent accounts are extracted from the adjusted trial balance to form a balance sheet.

Below is the balance sheet of Alpha Laundry Systems:

![]()

![]()

Activity 9

In this activity, the bookkeeper will be tasked to interpret financial statements (balance sheet, income statement, cash flow projection and summary of sales and cash receipts.

Normally it is not part of a bookkeeper’s job to analyze and interpret financial statement. It is the accountant’s job.

Below are some enrichments questions that need your computations and interpretations of balance sheet and income statement accounts of Alpha Laundry System for the month of June 2018.

1. Operating income ratio : Operating Income __________ = ____% Net Sales

Interpretation:_______________________________________________.

2. Return on asset (ROA) : Net Income __________ = _______% Ave. Assets

Interpretation:_______________________________________________.

3. Return on equity (ROE) : Net Income __________ = _______% Ave. Equity

Interpretation:_______________________________________________

4. Equity ratio : Total Equity __________ = _______%

Total Assets

Interpretation:______________________________________________.

![]()

Answer the following fill in blank questions:

1. ___________ is an employee of the company in charge to maintain bookkeeping records of the business.

2. ___________ Is considered the book of original entry.

3. ___________ Is considered the book of final entry.

4. ____________ Is a financial statement that reports the financial position of

the business.

5. ____________ Is a financial statement that reports net income or net loss of

the business.

6. ____________ Is an entry necessary to update ledger accounts from unadjusted trial balance to adjusted trial balance.

7. _____________ Is a report summarizing the ledger accounts with updated balances in debit and credit columns.

8. _____________ Is a statement that reports the cash inflow and cash outflow of the business.

9. _____________ Is a type of sales report that presents cash collection only.

10. _____________ Is a record that report cash inflow of the business.

![]()

GIN Janitorial and General Services, Inc., a company engaged in providing janitorial services to different business establishments in the city. The following financial data reveals the income and expenses records during the last quarter of 2018:

Revenue / Service Income:

|

Service rendered – on account (Deluxe Hotel) |

P95,000 |

|

||

|

Service rendered – Cash (Maxandria Hotel) |

45,000 |

|

||

|

Service rendered – on account (Pearlmont Inn) |

25,000 |

|

||

|

Service rendered – Cash (Mallberry Suites) |

105,000 |

|

||

|

Service rendered – Cash (VIP Hotel Inn) |

65,000 |

|

||

|

Service rendered – on account (Sogo Hotel) |

55,000 |

|

||

|

Service rendered – on account (Dynasty Court Hotel) |

75,000 |

|

||

|

Service rendered – on account (Grand City Hotel) |

60,000 |

|

||

|

|

------------------- |

||||

|

TOTAL |

P525,000 |

||||

|

Salaries and Wages of employees: |

|

||||

|

Janitor’s Salary – Total |

|

P 155,000 |

|||

|

Management staff salary-Total |

|

45,000 |

|||

|

General Manager’s salary – total |

|

90,000 |

|||

|

|

|

------------------- |

|||

|

TOTAL

Operating and administrative expenses:

|

|

P 290,000 |

|||

|

Utilities expenses |

|

P 15,000 |

|||

|

Rent expense |

|

15,000 |

|||

|

Repairs and Maintenance |

|

7,500 |

|||

|

Transportation and communications |

|

4,500 |

|||

|

Depreciation expense |

|

10,000 |

|||

|

|

|

------------------- |

|||

|

TOTAL |

|

P 52,000 |

|||

The owner of the business wants to know the operations of the business. You are tasked to compute for the following:

1. How much is the total service income collected in cash

2. How much is the total service income still collectible

3. How much is the total expenses

4. How much is the net income of GIN Janitorial and General Services, Inc.,

![]()

1. Measure the ability of the company to generate income from the use of its assets and invested capital as well as control its cost.

a. Solvency ratio c. Profitability ratio

b. Liquidity ratio d. Acid-test ratio

2. The following are financial records of ABC Corporation:

• Revenues – 20,000

• Rent expense – 3,000

• Salaries expense – 4,000

• Utilities expense – 2,000

How much is the total expenses?

|

a. P9,000 b. P10,000

3. How much is the net income? |

|

c. P 18,000 |

|

d. P1,000 |

|

a. P9,000 b. P10,000 |

|

c. P 18,000 |

|

d. P1,000 |

4. All of the following is an income statement accounts, except _________.

a. Rent expense c. Accounts receivable

b. Service fees d. Insurance expense

5. All of the following is a balance sheet accounts, except __________.

a. Cash c. Depreciation expense

b. Equipment d. Accumulated depreciation

6. One of the accounts title below is used in making an adjusting entry _________.

a. Liability c. Asset

b. Prepayments d. Capital

7. A financial statement that reports the Asset, Liability and Owner’s equity of the business is called ________.

a. Income statement c. General journal

b. Balance sheet d. General ledger

8. A financial statement that reports the Sales or Income received, Expenses and

the Net income of the business is called ________.

a. Income statement c. General journal

b. Balance sheet d. General ledger

9. Is a book used to record journal entries called the book of original entry is called _______.

a. Income statement c. General journal

b. Balance sheet d. General ledger

10. Is a book used to record account balances called the book of final entry is

called _______.

a. Income statement c. General journal

b. Balance sheet d. General ledger

Mr. Izatsuki Hamida, the bookkeeper of Honda Massage and Spa Services reported the following data for the month of January to March 2018:

Water expenses ---------------------- P 4,000

Soap expense ---------------------- 7,500

Massage oil expenses ---------------------- 15,000

Light & power expenses ---------------------- 12,000

Rent of the Massage parlor---------------------- 24,000

Salary of staff (4 massage worker)-------- 72,000 Income received from massage service-------- 120,000

Telephone expenses ------------------------ 7,500

How much is the net profit or net loss?

![]()

ACTIVITY 1

Generate an overall report of your business transactions.

1. Journal Entries

2. T- accounts

3. Trial Balance

4. Income Statement

5. Balance Sheet

ACTIVITY 2

PART I - Preparing personal income statement:

Things needed:

• Pen

• ¼ piece of paper (a note book sheet is ok)

• Calculator Instructions:

• Write your monthly allowance (computed by daily allowance x number of days in a month). Compute the total.

• Write the amount you spend on food, transportation, phone load, etc. (make it monthly to match their allowance). Compute the total.

• Deduct the total amount you spend from the total amount of your allowance.

• Associate allowance with revenue and spending with expense with the net amount as net income.

PART II - Preparing personal balance sheet:

Things needed:

• Pen

• ¼ piece of paper (a note book sheet is ok)

• Calculator

Instructions:

• Write your current savings and everything that they own (clothes, pen, pencil, etc.) Compute the total.

• Write the amount that you owed from your friends, family members, parents (tuition).

• Deduct the amount you owed from the amount they own.

• Associate the amounts owned with assets and amount owed with liabilities with the net amount as equity.

GROUP ACTIVITY: Compute your personal income:

Materials needed:

1. Ball pen

2. Meta cards - 3 colors (Green, Light Blue and Yellow) Or if not available, use any color

3. Calculator (cell phone is ok)

4. ½ White cartolina

5. Glue or scotch tape

Directions:

1. List down your income in Green meta card and compute the total

2. List down your expenses in yellow meta card and compute the total

3. Subtract the total amount computed in green meta card against the total amount computed in the yellow meta card.

4. Write the amount in the light meta card after the label “Net Profit” if the result of subtraction is positive. If the result is negative write “Net Loss”

5. Present it to the teacher when your name is called.

1. Which of the following is the process or activities by which a company adds value to an article, including production, marketing, and the provision of after-sales service?

A. 4Ms of production C. Value Chain

B. Supply Chain D. Business Model

2. Benjie is engaged in buying and selling shoes in his neighborhood. He gets his stocks from a local shoes dealer. Suppose each pair costs 1, 200.00 and Benjie add 50% mark-up. How much is the mark-up price?

A. 500.00 C. 700.00

B. 600.00 D. 800.00

3. Assuming no returns outwards or carriage inwards, the cost of goods sold will be equal to:

A. Sales less gross profit

B. Opening stock plus purchases plus closing stock

C. Closing stock less purchases plus opening stock

D. Purchases plus closing stock less opening stock

4. Which section of a business plan is generally first but written last?

A. Business description and vision

B. Appendices

C. Executive summary

D. Description of market

5. Is the process of evaluating risks, performance, financial health, and future prospects of a business by subjecting financial statement data to computational and analytical techniques with the objective of making economic decisions Horizontal analysis.

A. Horizontal analysis C. Ratio analysis

B. Vertical analysis D. Financial statement analysis

6. Statement I- Manpower in production operation refers to the workers involved in the production of goods.

Statement II- Machine refers to the raw materials needed in the production of a product.

A. Statement I is true. C. Both statements are true.

B. Statement II is true. D. Both statements are false

7. Costs incurred through payment of utilities such as electricity and water –

|

A. Revenue |

C. Free |

|

B. Mark-up

8. Gross profit less expenses is known as: |

D. Operating Expenses |

|

A. Total drawings |

C.Net turnover |

|

B. Cost of goods sold |

D. Net profit |

9. What is typical timeframe that a business plan addresses?

A. One year

B. the anticipated life of the business

C. At least three to five years

D. At least five years

10. Is a technique for evaluating a series of financial statement data over a period of time with the purpose of determining the increase or decrease that has taken place. Also called trend analysis.

A. Horizontal analysis C. Ratio analysis

B. Vertical analysis D. Financial statement analysis

11. Which of the following is a replica of a product as it will be manufactured, which may include such details as color, graphics, packaging and instructions?

A. Prototype C. Supplies

B. Materials D. Outputs

12. Which of the following is a system of organizations, people, activities, information, and resources involved in moving a product or service from supplier to customer?

A. Business Model C. Supply chain

B. Suppliers D. Value Chain

13. The selling price of an item or merchandise is computed by adding cost per unit and __________?

A. Revenue C. Discount

B. Mark Up D. Number of Items

14. It is a tool that allows managers to make educated estimates on revenue and costs of the business in order to cope up with uncertainties of the future –

A. Estimating C. Forecasting

B. Guessing D. Benchmarking

15. Net turnover can be calculated as:

A. Sales plus returns inwards

B. Gross profit plus cost of goods sold

C. Sales less returns outwards

D. Purchases plus opening stock less returns outwards

16. Which of the following would not appear in the profit and loss account?

A. Drawings C. Cash expenses.

B. Carriage outwards. D. Rent received

17. What is the biggest mistake you can make when preparing a business plan?

A. Not telling a compelling story

B. Forgetting the executive summary

C. Failing to include at least one appendix

D. Misrepresenting facts

E. Failing to have a clear vision of the business

18. This section will discuss information about your business, your goals and the customers you plan to serve.

A. Executive summary C. Marketing plan

B. Company description D. Financial projection

19. ________ is a technique that expresses each financial statement item as a percentage of a base amount. Also called common-size analysis.

A. Horizontal analysis C. Ratio analysis

B. Vertical analysis D. Financial statement analysis

20. Which of the following best describes recruitment?

A. tools to produce goods or to generate services

B. process by which a business seeks to hire the right person for a vacancy

C. marketing copy that explains what a product is and why it's worth purchasing

D. rationale of how an organization creates, delivers, and captures value in economic, social, cultural or other contexts

21. Which of the following is a set of procedures and instructions?

A. Value chain C. Manpower

B. Supply chain D. Methods

22. Claire is a fish vendor selling at the local public market. He gets his fish from a supplier at 100.00 pesos per kilo and sells it at160.00 45 per kilo to his customers. How much mark-up did Claire add to his selling price?

A. 40.00 C. 60.00

B. 50.00 D. 70.00

23. Refers to the amount added to the cost of a product to determine the selling price –

A. Revenue C. Mark Up

B. Cost D. Mark Down

24. The correct double-entry to transfer commission received for the year to the profit and loss account is:

|

The correct double-entry to transfer commission received for the year to the |

|||||

|

profit and loss account is: |

|

||||

|

|

Debit |

Credit |

|

|

|

A |

Trading |

Commission received |

|

|

|

B |

Commission received |

Profit and loss |

|

|

|

C |

Profit and loss |

Commission received |

|

|

|

D |

Commission received |

Trading |

|

|

25. What is an entrepreneur?

A. Someone who invests time and money to start a business.

B. Someone who makes a lot of money.

C. Someone who takes a risk to make a profit.

D. Both A & C.

26. This section of your business plan will show that you know the ins and outs of the industry and the specific market you are planning to enter.

A. Executive summary

B. Marketing plan

C. Competitive analysis

D. Market analysis

27. Your rival in the industry is called?

A. Competitor

B. Suppliers

C. Lending firms

D. Board of directors

28. Expresses the relationship among selected items of financial statement data. The relationship is expressed in terms of a percentage, a rate, or a simple proportion.

A. Horizontal analysis C. Ratio analysis

B. Vertical analysis D. Financial statement analysis

29. Statement I- A product description is the marketing copy that explains what a product is and why it's worth purchasing.

Statement II- Educational qualifications and experience is one of the criteria in considering manpower.

A. Statement I is false. C. Both statements are true.

B. Statement II is false. D. Both statements are false.

30. Statement I- Value chain is the process or activities by which a company adds value to an article, including production, marketing, and the provision of after-sales service.

Statement II- A supply chain is a system of organizations, people, activities, information, and resources involved in moving a product or service from supplier to customer.

A. Both statements are true. C. Statement I is false.

B. Both statements are false. D. none of the above.

31. Merchandise or goods purchased are referred to as –

A. Costs C. Expenses

B. Purchases D. Loss

32. Refers to goods and merchandise at the end of operation of business or accounting period.

A. Merchandise Inventory, end C. Expenses B. Freight-in D. Merchandise Inventory, beg.

33. Gross profit is the

A. Amount of money you get for profit lab. B. Amount of money collected from selling products C. Amount of money your product costs to produce

D. Has nothing to do with money

34. Net profit is the:

A. Amount of money you get for profit lab.

B. Amount of money collected from selling products.

C. Amount of money your product costs to produce.

D. Has nothing to do with money

35. The diagram showing your workers in the organization with their job responsibilities is called?

A. Organizational perspective

B. Organizational layout

C. Organizational chart

D. Organizational diagram

36. Promotional activity is found in which section of your business plan?

A. Management section

B. Financial section

C. Marketing section

D. Company description section

37. Measure the ability of the company to generate income from the use of its assets and invested capital as well as control its cost.

A. Solvency ratio C. Profitability ratio

B. Liquidity ratio D. Acid-test ratio

38. Statement I-. Output represents the final products from the production process and distributed to the customers.

Statement II- The 4Ms in the production operation are the materials, manpower, machine and money.

A. Both statements are true. C. Statement I is false.

B. Both statements are false. D. Statement II is false.

39. Which of the following is the marketing copy that explains what a product is and why it's worth purchasing?

A. Production method C. Business model

B. Product description D. Prototyping