|

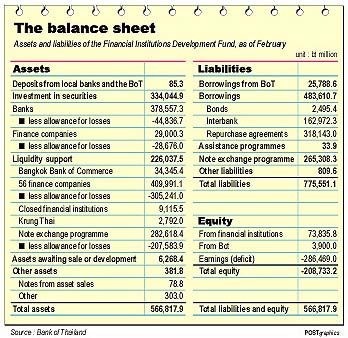

According to documents obtained by the Bangkok Post, losses for the Financial Institutions Development Fund totalled 286 billion baht as of February. Liabilities stood at 775.55 billion baht against assets of 566.8 billion, excluding additional contingent liabilities of 148.35 billion. The government absorbed 500 billion baht in losses of the fund in mid-1998 through the issue of state bonds. One economist said pressing the central bank to issue bonds for the debt of the development fund would hurt monetary discipline. "The Finance Ministry has said that it will control public debt from financial sector reform to 10% of the total budget, but the central bank governor said in London that the debt will rise to 21% of the total budget in 2004," he said.

|

"So there's a difference of 11% which the two parties are throwing between each other."The fiscal costs should be taken by the government, as central bank resources were not sufficient to finance the debt, the economist said. Some 90% of the central bank's profits are turned over to the Finance Ministry to meet interest costs on already-issued bonds. Another point was that the majority of excess reserves at the central bank reflected the baht's depreciation since mid-1997, and could decline if the currency appreciated in the future. Forcing the central bank to accept the losses would press the regulators to issue new bonds, leading to a conflict-of-interest for the central bank in managing inflation and monetary policy.

Another economist at the Thai Farmers Research Centre said the government should be cautious in dealing with the country's foreign reserves. "Basing on existing data, we still believe that dealing with the reserves in a conservative manner would be more acceptable and better strengthen investor confidence," he said. Issuing new bonds to finance the debt would raise the country's debt burden to around 70% of gross domestic product. While high, the costs were bearable, the economist said. One analyst said that offsetting the fund's losses posed a dilemma. If the central bank was forced to absorb such the losses, it would have to issue bonds, then causing inflation pressure to the money market.

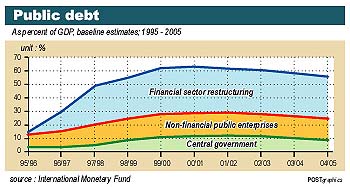

On the other hand, if the Finance Ministry shouldered the losses, there would be a tax burden for the public. "The dilemma is either we shoulder "fiscal tax" or "inflation tax". The Finance Ministry and the central bank plan to hold a public seminar in mid-May to debate options in restructuring the losses of the development fund. Both sides agree that the country's public debt is a key issue. According to the International Monetary Fund, the total debt has risen from just 15% of gross domestic product in 1995 to around 56% in 1998. Falling tax revenue and the need to maintain fiscal spending to ease the impact of the crisis have caused the government to run deficits for four consecutive years. But the biggest factor in growth of public debt has been financial restructuring, including costs incurred from the bail-out of ailing banks and finance companies.

M.R. Chatumongol, in a speech to investors in London earlier this month, noted that debt service costs reached 9.1% of last year's budget. "No matter how we reasonably finance the debt of FIDF, it does seem that the peak debt service will not exceed 21.7 % of the budget in the year 2004, even if we do not roll over domestic and external debt falling due in that year," he said. M.R. Chatumongol said if the central bank was weakened, even though fiscal debt was reduced, the overall result was likely a "a self-defeating proposition, because a weak central bank would cause much more of a problem than a large fiscal burden".

Most economists agree that the country's debt burden is sustainable. The International Monetary Fund, for instance, expects the public debt to peak at around 64% of GDP in 2000/01, then falling to 57% by 2004/05. The debt-to-GDP ratio is expected to reverse based on a consolidation in government deficits and the positive impact of GDP growth. The World Bank, estimates the total public debt, including fiscal costs of financial restructuring, at around 71% of GDP by the end of the year.

"Despite these high costs, however, preliminary projections suggest that public debt dynamics is sustainable, if the government manages to generate a primary fiscal surplus of 2% of GDP starting in 2003," the World Bank said in a March report.